There’s Always Something to Do: The Peter Cundill Investment Approach, by Christopher Risso-Gill (2011), is an excellent book. Cundill was a highly successful deep value investor whose chosen method was to buy stocks below their liquidation value.

Here is an outline for this blog post:

Peter Cundill

Getting to First Base

Launching a Value Fund

Value Investment in Action

Going Global

A Decade of Success

Investments and Stratagems

Learning From Mistakes

Entering the Big League

There’s Always Something Left to Learn

Pan Ocean

Fragile X

What Makes a Great Investor?

Glossary of Terms with Cundill’s Comments

PETER CUNDILL

It was December in 1973 when Peter Cundill first discovered value investing. He was 35 years old at the time. Up until then, despite a great deal of knowledge and experience, Cundill hadn’t yet discovered an investment strategy. He happened to be reading George Goodman’s Super Money on a plane when he came across chapter 3 on Benjamin Graham and Warren Buffett. Cundill wrote about his epiphany that night in his journal:

…there before me in plain terms was the method, the solid theoretical back-up to selecting investments based on the principle of realizable underlying value. My years of apprenticeship were over: ‘THIS IS WHAT I WANT TO DO FOR THE REST OF MY LIFE!’

What particularly caught Cundill’s attention was Graham’s notion that a stock is cheap if it sells below liquidation value. The farther below liquidation value the stock is, the higher the margin of safety and the higher the potential returns. This idea is at odds with modern finance theory, according to which getting higher returns always requires taking more risk.

Peter Cundill became one of the best value investors in the world. He followed a deep value strategy based entirely on buying companies below their liquidation values.

We do liquidation analysis and liquidation analysis only.

GETTING TO FIRST BASE

One of Cundill’s first successful investments was in Bethlehem Copper. Cundill built up a position at $4.50, roughly equal to cash on the balance sheet and far below liquidation value:

Both Bethlehem and mining stocks in general were totally out of favour with the investing public at the time. However in Peter’s developing judgment this was not just an irrelevance but a positive bonus. He had inadvertently stumbled upon a classic net-net: a company whose share price was trading below its working capital, net of all its liabilities. It was the first such discovery of his career and had the additional merit of proving the efficacy of value theory almost immediately, had he been able to recognize it as such. Within four months Bethlehem had doubled and in six months he was able to start selling some of the position at $13.00. The overall impact on portfolio performance had been dramatic.

Riso-Gill describes Cundill as having boundless curiosity. Cundill would not only visit the worst performing stock market in the world near the end of each year in search of bargains. But he also made a point of total immersion with respect to the local culture and politics of any country in which he might someday invest.

LAUNCHING A VALUE FUND

Early on, Cundill had not yet developed the deep value approach based strictly on buying below liquidation value. He had, however, concluded that most models used in investment research were useless and that attempting to predict the general stock market was not doable with any sort of reliability. Eventually Cundill immersed himself in Graham and Dodd’s Security Analysis, especially chapter 41, “The Asset-Value Factor in Common-Stock Valuation,” which he re-read and annotated many times.

When Cundill was about to take over an investment fund, he wrote to the shareholders about his proposed deep value investment strategy:

The essential concept is to buy under-valued, unrecognized, neglected, out of fashion, or misunderstood situations where inherent value, a margin of safety, and the possibility of sharply changing conditions created new and favourable investment opportunities. Although a large number of holdings might be held, performance was invariably established by concentrating in a few holdings. In essence, the fund invested in companies that, as a result of detailed fundamental analysis, were trading below their ‘intrinsic value.’ The intrinsic value was defined as the price that a private investor would be prepared to pay for the security if it were not listed on a public stock exchange. The analysis was based as much on the balance sheet as it was on the statement of profit and loss.

Cundill went on to say that he would only buy companies trading below book value, preferably below net working capital less long term debt (Graham’s net-net method). Cundill also required that the company be profitable–ideally having increased its earnings for the past five years–and dividend-paying–ideally with a regularly increasing dividend. The price had to be less than half its former high and preferably near its all time low. And the P/E had to be less than 10.

Cundill also studied past and future profitability, the ability of management, and factors governing sales volume and costs. But Cundill made it clear that the criteria were not always to be followed precisely, leaving room for investment judgment, which he eventually described as an art form.

Cundill told shareholders about his own experience with the value approach thus far. He had started with $600,000, and the portfolio increased 35.2%. During the same period, the All Canadian Venture Fund was down 49%, the TSE industrials down 20%, and the Dow down 26%. Cundill also notes that 50% of the portfolio had been invested in two stocks (Bethlehem Copper and Credit Foncier).

About this time, Irving Kahn became a sort of mentor to Cundill. Kahn had been Graham’s teaching assistant at Columbia University.

VALUE INVESTMENT IN ACTION

Having a clearly defined set of criteria helped Cundill to develop a manageable list of investment candidates in the decade of 1974 to 1984 (which tended to be a good time for value investors). The criteria also helped him identify a number of highly successful investments.

For example, the American Investment Company (AIC), one of the largest personal loan companies in the United States, saw its stock fall from over $30.00 to $3.00, despite having a tangible book value per share of $12.00. As often happens with good contrarian value candidates, the fears of the market about AIC were overblown. Eventually the retail loan market recovered, but not before Cundill was able to buy 200,000 shares at $3.00. Two years later, AIC was taken over at $13.00 per share by Leucadia. Cundill wrote:

As I proceed with this specialization into buying cheap securities I have reached two conclusions. Firstly, very few people really do their homework properly, so now I always check for myself. Secondly, if you have confidence in your own work, you have to take the initiative without waiting around for someone else to take the first plunge.

…I think that the financial community devotes far too much time and mental resource to its constant efforts to predict the economic future and consequent stock market beaviour using a disparate, and almost certainly incomplete, set of statistical variables. It makes me wonder what might be accomplished if all this time, energy, and money were to be applied to endeavours with a better chance of proving reliable and practically useful.

Meanwhile, Cundill had served on the board of AIC, which brought some valuable experience and associations.

Cundill found another highly discounted company in Tiffany’s. The company owned extremely valuable real estate in Manhattan that was carried on its books at a cost much lower than the current market value. Effectively, the brand was being valued at zero. Cundill accumulated a block of stock at $8.00 per share. Within a year, Cundill was able to sell it at $19.00. This seemed like an excellent result, except that six months later, Avon Products offered to buy Tiffany’s at $50.00. Cundill would comment:

The ultimate skill in this business is in knowing when to make the judgment call to let profits run.

Sam Belzberg–who asked Cundill to join him as his partner at First City Financial–described Cundill as follows:

He has one of the most important attributes of the master investor because he is supremely capable of running counter to the herd. He seems to possess the ability to consider a situation in isolation, cutting himself off from the mill of general opinion. And he has the emotional confidence to remain calm when events appear to be indicating that he’s wrong.

GOING GLOBAL

Partly because of his location in Canada, Cundill early on believed in global value investing. He discovered that just as individual stocks can be neglected and misunderstood, so many overseas markets can be neglected and misunderstood. Cundill enjoyed traveling to these various markets and learning the legal accounting practices. In many cases, the difficulty of mastering the local accounting was, in Cundill’s view, a ‘barrier to entry’ to other potential investors.

Cundill also worked hard to develop networks of locally based professionals who understood value investing principles. Eventually, Cundill developed the policy of exhaustively searching the globe for value, never favoring domestic North American markets.

A DECADE OF SUCCESS

Cundill summarized the lessons of the first 10 years, during which the fund grew at an annual compound rate of 26%. He included the following:

The value method of investing will tend at least to give compound rates of return in the high teens over longer periods of time.

There will be losing years; but if the art of making money is not to lose it, then there should not be substantial losses.

The fund will tend to do better in slightly down to indifferent markets and not to do as well as our growth-oriented colleagues in good markets.

It is ever more challenging to perform well with a larger fund…

We have developed a network of contacts around the world who are like-minded in value orientation.

We have gradually modified our approach from a straight valuation basis to one where we try to buy securities selling below liquidation value, taking into consideration off-balance sheet items.

THE MOST IMPORTANT ATTRIBUTE FOR SUCCESS IN VALUE INVESTING IS PATIENCE, PATIENCE, AND MORE PATIENCE. THE MAJORITY OF INVESTORS DO NOT POSSESS THIS CHARACTERISTIC.

INVESTMENTS AND STRATAGEMS

Buying at a discount to liquidation value is simple in concept. But in practice, it is not at all easy to do consistently well over time. Peter Cundill explained:

None of the great investments come easily. There is almost always a major blip for whatever reason and we have learnt to expect it and not to panic.

Although Cundill focused exclusively on discount to liquidation value when analyzing equities, he did develop a few additional areas of expertise, such as distressed debt. Cundill discovered that, contrary to his expectation of fire-sale prices, an investor in distressed securities could often achieve large profits during the actual process of liquidation. Success in distressed debt required detailed analysis.

LEARNING FROM MISTAKES

1989 marked the fifteenth year in a row of positive returns for Cundill’s Value Fund. The compound growth rate was 22%. But the fund was only up 10% in 1989, which led Cundill to perform his customary analysis of errors:

…How does one reduce the margin of error while recognizing that investments do, of course, go down as well as up? The answers are not absolutely clear cut but they certainly include refusing to compromise by subtly changing a question so that it shapes the answer one is looking for, and continually reappraising the research approach, constantly revisiting and rechecking the detail.

What were last year’s winners? Why?–I usually had the file myself, I started with a small position and stayed that way until I was completely satisfied with every detail.

For most value investors, the investment thesis depends on a few key variables, which should be written down in a short paragraph. It’s important to recheck each variable periodically. If any part of the thesis has been invalidated, you must reassess. Usually the stock is no longer a bargain.

It’s important not to invent new reasons for owning the stock if one of the original reasons has been falsified. Developing new reasons for holding a stock is usually misguided. However, you need to remain flexible. Occasionally the stock in question is still a bargain.

ENTERING THE BIG LEAGUE

In the mid 1990’s, Cundill made a large strategic shift out of Europe and into Japan. Typical for a value investor, he was out of Europe too early and into Japan too early. Cundill commented:

We dined out in Europe, we had the biggest positions in Deutsche Bank and Paribas, which both had big investment portfolios, so you got the bank itself for nothing. You had a huge margin of safety–it was easy money. We had doubles and triples in those markets and we thought we were pretty smart, so in 1996 and 1997 we took our profits and took flight to Japan, which was just so beaten up and full of values. But in doing so we missed out on some five baggers, which is when the initial investment has multiplied five times, and we had to wait at least two years before Japan started to come good for us.

This is a recurring problem for most value investors–that tendency to buy and to sell too early. The virtues of patience are severely tested and you get to thinking it’s never going to work and then finally your ship comes home and you’re so relieved that you sell before it’s time. What we ought to do is go off to Bali or some such place and sit in the sun to avoid the temptation to sell too early.

As for Japan, Cundill had long ago learned the lesson that cheap stocks can stay cheap for “frustratingly long” periods of time. Nonetheless, Cundill kept loading up on cheap Japanese stocks in a wide range of sectors. In 1999, his Value Fund rose 16%, followed by 20% in 2000.

THERE’S ALWAYS SOMETHING LEFT TO LEARN

Although Cundill had easily avoided Nortel, his worst investment was nevertheless in telecommunications: Cable & Wireless (C&W). In the late 1990’s, the company had to give up many of its networks in newly independent former British colonies. The shares dropped from 15 pounds per share to 6 pounds.

A new CEO, Graham Wallace, was brought in. He quickly and skillfully negotiated a series of asset sales, which dramatically transformed the balance sheet from net debt of 4 billion pounds to net cash of 2.6 billion pounds. Given the apparently healthy margin of safety, Cundill began buying shares in March 2000 at just over 4 pounds per share. (Net asset value was 4.92 pounds per share.) Moreover:

[Wallace was] generally regarded as a relatively safe pair of hands unlikely to be tempted into the kind of acquisition spree overseen by his predecessor.

Unfortunately, a stream of investment bankers, management consultants, and brokers made a simple but convincing pitch to Wallace:

the market for internet-based services was growing at three times the rate for fixed line telephone communications and the only quick way to dominate that market was by acquisition.

Wallace proceeded to make a series of expensive acquisitions of loss-making companies. This destroyed C&W’s balance sheet and also led to large operating losses. Cundill now realized that the stock could go to zero, and he got out, just barely. As Cundill wrote later:

… So we said, look they’ve got cash, they’ve got a valuable, viable business and let’s assume the fibre optic business is worth zero–it wasn’t, it was worth less than zero, much, much less!

Cundill had invested nearly $100 million in C&W, and they lost nearly $59 million. This loss was largely responsible for the fund being down 11% in 2002. Cundill realized that his investment team needed someone to be a sceptic for each potential investment.

PAN OCEAN

In late 2002, oil prices began to rise sharply based on global growth. Cundill couldn’t find any net-net’s among oil companies, so he avoided these stocks. Some members of his investment team argued that there were some oil companies that were very undervalued. Finally, Cundill announced that if anyone could find an oil company trading below net cash, he would buy it.

Cundill’s cousin, Geoffrey Scott, came across a neglected company: Pan Ocean Energy Corporation Ltd. The company was run by David Lyons, whose father, Vern Lyons, had founded Ocelot Energy. Lyons concluded that there was too much competition for a small to medium sized oil company operating in the U.S. and Canada. The risk/reward was not attractive.

What he did was to merge his own small Pan Ocean Energy with Ocelot and then sell off Ocelot’s entire North American and other peripheral parts of the portfolio, clean up the balance sheet, and bank the cash. He then looked overseas and determined that he would concentrate on deals in Sub-Saharan Africa, where licenses could be secured for a fraction of the price tag that would apply in his domestic market.

Lyons was very thorough and extremely focused… He narrowed his field down to Gabon and Tanzania and did a development deal with some current onshore oil production in Gabon and a similar offshore gas deal in Tanzania. Neither was expensive.

Geoffrey Scott examined Pan Ocean, and found that its share price was almost equal to net cash and the company had no debt. He immediately let Cundill know about it. Cundill met with David Lyons and was impressed:

This was a cautious and disciplined entrepreneur, who was dealing with a pool of cash that in large measure was his own.

Lyons invited Cundill to see the Gabon project for himself. Eventually, Cundill saw both the Gabon project and the Tanzania project. He liked what he saw. Cundill’s fund bought 6% of Pan Ocean. They made six times their money in two and a half years.

FRAGILE X

As early as 1998, Cundill had noticed a slight tremor in his right arm. The condition worsened and affected his balance. Cundill continued to lead a very active life, still reading and traveling all the time, and still a fitness nut. He was as sharp as ever in 2005. Risso-Gill writes:

Ironically, just as Peter’s health began to decline an increasing number of industry awards for his achievements started to come his way.

For instance, he received the Analyst’s Choice award as “The Greatest Mutual Fund Manager of All Time.”

In 2009, Cundill decided that it was time to step down, as his condition had progressively worsened. He continued to be a voracious reader.

WHAT MAKES A GREAT INVESTOR?

Risso-Gill tries to distill from Cundill’s voluminous journal writings what Cundill himself believed it took to be a great value investor.

INSATIABLE CURIOSITY

Curiosity is the engine of civilization. If I were to elaborate it would be to say read, read, read, and don’t forget to talk to people, really talk, listening with attention and having conversations, on whatever topic, that are an exchange of thoughts. Keep the reading broad, beyond just the professional. This helps to develop one’s sense of perspective in all matters.

PATIENCE

Patience, patience, and more patience…

CONCENTRATION

You must have the ability to focus and to block out distractions. I am talking about not getting carried away by events or outside influences–you can take them into account, but you must stick to your framework.

ATTENTION TO DETAIL

Never make the mistake of not reading the small print, no matter how rushed you are. Always read the notes to a set of accounts very carefully–they are your barometer… They will give you the ability to spot patterns without a calculator or spreadsheet. Seeing the patterns will develop your investment insights, your instincts–your sense of smell. Eventually it will give you the agility to stay ahead of the game, making quick, reasoned decisions, especially in a crisis.

CALCULATED RISK

… Either [value or growth investing] could be regarded as gambling, or calculated risk. Which side of that scale they fall on is a function of whether the homework has been good enough and has not neglected the fieldwork.

INDEPENDENCE OF MIND

I think it is very useful to develop a contrarian cast of mind combined with a keen sense of what I would call ‘the natural order of things.’ If you can cultivate these two attributes you are unlikely to become infected by dogma and you will begin to have a predisposition toward lateral thinking–making important connections intuitively.

HUMILITY

I have no doubt that a strong sense of self belief is important–even a sense of mission–and this is fine as long as it is tempered by a sense of humour, especially an ability to laugh at oneself. One of the greatest dangers that confront those who have been through a period of successful investment is hubris–the conviction that one can never be wrong again. An ability to see the funny side of oneself as it is seen by others is a strong antidote to hubris.

ROUTINES

Routines and discipline go hand in hand. They are the roadmap that guides the pursuit of excellence for its own sake. They support proper professional ambition and the commercial integrity that goes with it.

SCEPTICISM

Scepticism is good, but be a sceptic, not an iconoclast. Have rigour and flexibility, which might be considered an oxymoron but is exactly what I meant when I quoted Peter Robertson’s dictum ‘always change a winning game.’ An investment framework ought to include a liberal dose of scepticism both in terms of markets and of company accounts.

PERSONAL RESPONSIBILITY

The ability to shoulder personal responsibility for one’s investment results is pretty fundamental… Coming to terms with this reality sets you free to learn from your mistakes.

GLOSSARY OF TERMS WITH CUNDILL’S COMMENTS

Here are some of the terms.

ANALYSIS

There’s almost too much information now. It boggles most shareholders and a lot of analysts. All I really need is a company’s published reports and records, that plus a sharp pencil, a pocket calculator, and patience.

Doing the analysis yourself gives you confidence buying securities when a lot of the external factors are negative. It gives you something to hang your hat on.

ANALYSTS

I’d prefer not to know what the analysts think or to hear any inside information. It clouds one’s judgment–I’d rather be dispassionate.

BROKERS

I go cold when someone tips me on a company. I like to start with a clean sheet: no one’s word. No givens. I’m more comfortable when there are no brokers looking over my shoulder.

They really can’t afford to be contrarians. A major investment house can’t afford to do research for five customers who won’t generate a lot of commissions.

EXTRA ASSETS

This started for me when Mutual Shares chieftain Mike Price, who used to be a pure net-net investor, began talking about something called the ‘extra asset syndrome’ or at least that is what I call it. It’s taking, you might say, net-net one step farther, to look at all of a company’s assets, figure the true value.

FORECASTING

We don’t do a lot of forecasting per se about where markets are going. I have been burned often enough trying.

INDEPENDENCE

Peter Cundill has never been afraid to make his own decisions and by setting up his own fund management company he has been relatively free from external control and constraint. He doesn’t follow investment trends or listen to the popular press about what is happening on ‘the street.’ He has travelled a lonely but profitable road.

‘Being willing to be the only one in the parade that’s out of step. It’s awfully hard to do, but Peter is disciplined. You have to be willing to wear bellbottoms when everyone else is wearing stovepipes.‘ – Ross Southam

INVESTMENT FORMULA

Mostly Graham, a little Buffett, and a bit of Cundill.

I like to think that if I stick to my formula, my shareholders and I can make a lot of money without much risk.

When I stray out of my comfort zone I usually get my head handed to me on a platter.

I suspect that my thinking is an eclectic mix, not pure net-net because I couldn’t do it anyway so you have to have a new something to hang your hat on. But the framework stays the same.

INVESTMENT STRATEGY

I used to try and pick the best stocks in the fund portfolios, but I always picked the wrong ones. Now I take my own money and invest it with that odd guy Peter Cundill. I can be more detached when I treat myself as a normal client.

If it is cheap enough, we don’t care what it is.

Why will someone sell you a dollar for 50 cents? Because in the short run, people are irrational on both the optimistic and pessimistic side.

MANTRAS

All we try to do is buy a dollar for 40 cents.

In our style of doing things, patience is patience is patience.

One of the dangers about net-net investing is that if you buy a net-net that begins to lose money your net-net goes down and your capacity to be able to make a profit becomes less secure. So the trick is not necessarily to predict what the earnings are going to be but to have a clear conviction that the company isn’t going bust and that your margin of safety will remain intact over time.

MARGIN OF SAFETY

The difference between the price we pay for a stock and its liquidation value gives us a margin of safety. This kind of investing is one of the most effective ways of achieving good long-term results.

MARKETS

If there’s a bad stock market, I’ll inevitably go back in too early. Good times last longer than we think but so do bad times.

Markets can be overvalued and keep getting expensive, or undervalued and keep getting cheap. That’s why investing is an art form, not a science.

I’m agnostic on where the markets will go. I don’t have a view. Our task is to find undervalued global securities that are trading well below their intrinsic value. In other words, we follow the strict Benjamin Graham approach to investing.

NEW LOWS

Search out the new lows, not the new highs. Read the Outstanding Investor Digest to find out what Mason Hawkins or Mike Price is doing. You know good poets borrow and great poets steal. So see what you can find. General reading–keep looking at the news to see what’s troubled. Experience and curiosity is a really winning combination.

What differentiates us from other money managers with a similar style is that we’re comfortable with new lows.

NOBODY LISTENING

Many people consider value investing dull and as boring as watching paint dry. As a consequence value investors are not always listened to, especially in a stock market bubble. Investors are often in too much of a hurry to latch on to growth stocks to stop and listen because they’re afraid of being left out…

OSMOSIS

I don’t just calculate value using net-net. Actually there are many different ways but you have to use what I call osmosis–you have got to feel your way. That is the art form, because you are never going to be right completely; there is no formula that will ever get you there on its own. Osmosis is about intuition and about discipline and about all the other things that are not quantifiable. So can you learn it? Yes, you can learn it, but it’s not a science, it’s an art form. The portfolio is a canvas to be painted and filled in.

PATIENCE

When times aren’t good I’m still there. You find bargains among the unpopular things, the things that everybody hates. The key is that you must have patience.

RISK

We try not to lose. But we don’t want to try too hard. The losses, of course, work against you in establishing decent compound rates of return. And I hope we won’t have them. But I don’t want to be so risk-averse that we are always trying too hard not to lose.

STEADY RETURNS

All I know is that if you can end up with a 20% track record over a longer period of time, the compound rates of return are such that the amounts are staggering. But a lot of investors want excitement, not steady returns. Most people don’t see making money as grinding it out, doing it as efficiently as possible. If we have a strong market over the next six months and the fund begins to drop behind and there isn’t enough to do, people will say Cundill’s lost his touch, he’s boring.

TIMING: “THERE’S ALWAYS SOMETHING TO DO”

…Irving Kahn gave me some advice many years ago when I was bemoaning the fact that according to my criteria there was nothing to do. He said, ‘there is always something to do. You just need to look harder, be creative and a little flexible.’

VALUE INVESTING

I don’t think I want to become too fashionable. In some ways, value investing is boring and most investors don’t want a boring life–they want some action: win, lose, or draw.

I think the best decisions are made on the basis of what your tummy tells you. The Jesuits argue reason before passion. I argue reason and passion. Intellect and intuition. It’s a balance.

We do liquidation analysis and liquidation analysis only.

Ninety to 95% of all my investing meets the Graham tests. The times I strayed from a rigorous application of this philosophy I got myself into trouble.

But what do you do when none of these companies is available? The trick is to wait through the crisis stage and into the boredom stage. Things will have settled down by then and values will be very cheap again.

We customarily do three tests: one of them asset-based–the NAV, using the company’s balance sheet. The second is the sum of the parts, which I think is probably the most important part that goes into the balance sheet I’m creating. And then a future NAV, which is making a stab (which I am always suspicious about) at what you think the business might be doing in three years from now.

WORKING LIFE

I’ve been doing this for thirty years. And I love it. I’m lucky to have the kind of life where the differentiation between work and play is absolutely zilch. I have no idea whether I’m working or whether I’m playing.

My wife says I’m a workaholic, but my colleagues say I haven’t worked for twenty years. My work is my play.

BOOLE MICROCAP FUND

An equal weighted group of micro caps generally far outperforms an equal weighted (or cap-weighted) group of larger stocks over time. See the historical chart here: https://boolefund.com/best-performers-microcap-stocks/

This outperformance increases significantly by focusing on cheap micro caps. Performance can be further boosted by isolating cheap microcap companies that show improving fundamentals. We rank microcap stocks based on these and similar criteria.

There are roughly 10-20 positions in the portfolio. The size of each position is determined by its rank. Typically the largest position is 15-20% (at cost), while the average position is 8-10% (at cost). Positions are held for 3 to 5 years unless a stock approachesintrinsic value sooner or an error has been discovered.

The mission of the Boole Fund is to outperform the S&P 500 Index by at least 5% per year (net of fees) over 5-year periods. We also aim to outpace the Russell Microcap Index by at least 2% per year (net). The Boole Fund has low fees.

If you are interested in finding out more, please e-mail me or leave a comment.

My e-mail: jb@boolefund.com

Disclosures: Past performance is not a guarantee or a reliable indicator of future results. All investments contain risk and may lose value. This material is distributed for informational purposes only. Forecasts, estimates, and certain information contained herein should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed.No part of this article may be reproduced in any form, or referred to in any other publication, without express written permission of Boole Capital, LLC.

Nassim Nicholas Taleb’sFooled by Randomness: The Hidden Role of Chance in the Markets and in Life, is an excellent book. Below I summarize the main points.

Here’s the outline:

Prologue

Part I: Solon’s Warning–Skewness, Asymmetry, and Induction

One: If You’re So Rich, Why Aren’t You So Smart?

Two: A Bizarre Accounting Method

Three: A Mathematical Meditation on History

Four: Randomness, Nonsense, and the Scientific Intellectual

Five: Survival of the Least Fit–Can Evolution Be Fooled By Randomness?

Six: Skewness and Asymmetry

Seven: The Problem of Induction

Part II: Monkeys on Typewriters–Survivorship and Other Biases

Eight: Too Many Millionaires Next Door

Nine: It Is Easier to Buy and Sell Than Fry an Egg

Ten: Loser Takes All–On the Nonlinearities of Life

Eleven: Randomness and Our Brain–We Are Probability Blind

Part III: Wax in my Ears–Living With Randomitis

Twelve: Gamblers’ Ticks and Pigeons in a Box

Thirteen: Carneades Comes to Rome–On Probability and Skepticism

Fourteen: Bacchus Abandons Antony

(Albrecht Durer’sWheel of Fortunefrom Sebastien Brant’sShip of Fools(1494) via Wikimedia Commons)

PROLOGUE

Taleb presents Table P.1 Table of Confusion, listing the central distinctions used in the book.

GENERAL

Luck

Skills

Randomness

Determinism

Probability

Certainty

Belief, conjecture

Knowledge, certitude

Theory

Reality

Anecdote, coincidence

Causality, law

Forecast

Prophecy

MARKET PERFORMANCE

Lucky idiot

Skilled investor

Survivorship bias

Market outperformance

FINANCE

Volatility

Return (or drift)

Stochastic variable

Deterministic variable

PHYSICS AND ENGINEERING

Noise

Signal

LITERARY CRITICISM

None

Symbol

PHILOSOPHY OF SCIENCE

Epistemic probability

Physical probability

Induction

Deduction

Synthetic proposition

Analytic proposition

ONE: IF YOU’RE SO RICH, WHY AREN’T YOU SO SMART?

Taleb introduces an options trader Nero Tulip. He became convinced that being an options trader was even more interesting that being a pirate would be.

Nero is highly educated (like Taleb himself), with an undergraduate degree in ancient literature and mathematics from Cambridge University, a PhD. in philosophy from the University of Chicago, and a PhD. in mathematical statistics. His thesis for the PhD. in philosophy had to do with the methodology of statistical inference in its application to the social sciences. Taleb comments:

In fact, his thesis was indistinguishable from a thesis in mathematical statistics–it was just a bit more thoughtful (and twice as long).

Nero left philosophy because he became bored with academic debates, particularly over minor points. Nero wanted action.

(Photo by Neil Lockhart)

Nero became a proprietary trader. The firm provided the capital. As long as Nero generated good results, he was free to work whenever he wanted. Generally he was allowed to keep between 7% and 12% of his profits.

It is paradise for an intellectual like Nero who dislikes manual work and values unscheduled meditation.

Nero was an extremely conservative options trader. Over his first decade, he had almost no bad years and his after-tax income averaged $500,000. Due to his extreme risk aversion, Nero’s goal is not to maximize profits as much as it is to avoid having such a bad year that his “entertaining money machine called trading” would be taken away from him. In other words, Nero’s goal was to avoidblowing up, or having such a bad year that he would have to leave the business.

Nero likes taking small losses as long as his profits are large. Whereas most traders make money most of the time during a bull market and lose money during market panics or crashes, Nero would lose small amounts most of the time during a bull market and then make large profits during a market panic or crash.

Nero does not do as well as some other traders. One reason is that his extreme risk aversion leads him to invest his own money in treasury bonds. So he missed most of the bull market from 1982 to 2000.

Note: From a value investing point of view, Nero should at least have invested in undervalued stocks, since such a strategy will almost certainly do well after 10+ years. But Nero wasn’t trained in value investing, and he was acutely aware of what can happen during market panics or crashes.

Also Note: For a value investor, a market panic or crash is an opportunity to buy more stock at very cheap prices. Thus bear markets benefit the value investor who can add to his or her positions.

Nero and his wife live across the street from John the High-Yield Trader and his wife. John was doing much better than Nero. John’s strategy was to maximize profits for as long as the bull market lasted. Nero’s wife and even Nero himself would occasionally feel jealous when looking at the much larger house in which John and his wife lived. However, one day there was a market panic and Johnblew up, losing virtually everything including his house.

Taleb writes:

…Nero’s merriment did not come from the fact that John went back to his place in life, so much as it was from the fact that Nero’s methods, beliefs, and track record had suddenly gained in credibility. Nero would be able to raise public money on his track record precisely because such a thing could not possibly happen to him. A repetition of such an event would pay off massively for him. Part of Nero’s elation also came from the fact that he felt proud of his sticking to his strategy for so long, in spite of the pressure to be the alpha male. It was also because he would no longer question his trading style when others were getting rich because they misunderstood the structure of randomness and market cycles.

Taleb then comments that lucky fools never have the slightest suspicion that they are lucky fools. As long as they’re winning, they get puffed up from the release of the neurotransmitter serotonin into their systems. Taleb notes that our hormonal system can’t distinguish between winning based on luck and winning based on skill.

(A lucky seven. Photo by Eagleflying)

Furthermore, when serotonin is released into our system based on some success, we act like we deserve the success, regardless of whether it was based on luck or skill. Our new behavior will often lead to a virtuous cycle during which, if we continue to win, we will rise in the pecking order. Similarly, when we lose, whether that loss is due to bad luck or poor skill, our resulting behavior will often lead to a vicious cycle during which, if we continue to lose, we will fall in the pecking order. Taleb points out that these virtuous and vicious cycles are exactly what happens with monkeys who have been injected with serotonin.

Taleb adds that you can always tell whether some trader has had a winning day or a losing day. You just have to observe his or her gesture or gait. It’s easy to tell whether the trader is full of serotonin or not.

Photo by Antoniodiaz

TWO: A BIZARRE ACCOUNTING METHOD

Taleb introduces the concept ofalternative histories. This concept applies to many areas of human life, including many different professions (war, politics, medicine, investments). The main idea is that you cannot judge the quality of a decision based only on its outcome. Rather, the quality of a decision can only be judged by considering all possible scenarios (outcomes) and their associated probabilities.

Once again, our brains deceive us unless we develop the habit of thinking probabilistically, in terms of alternative histories. Without this habit, if a decision is successful, we get puffed up with serotonin and believe that the successful outcome is based on our skill. By nature, we cannot account for luck or randomness.

Taleb offers Russian roulette as an analogy. If you are offered $10 million to play Russian roulette, and if you play and you survive, then you were lucky even though you will get puffed up with serotonin.

Photo by Banjong Khanyai

Taleb argues that many (if not most) business successes have a large component of luck or randomness. Again, though, successful businesspeople in general will be puffed up with serotonin and they will attribute their success primarily to skill. Taleb:

…the public observes the external signs of wealth without even having a glimpse at the source (we call such source thegenerator).

Now, if the lucky Russian roulette player continues to play the game, eventually the bad histories will catch up with him or her. Here’s an important point: If you start out with thousands of people playing Russian roulette, then after the first round roughly 83.3% will be successful. After the second round, roughly 83.3% of the survivors of round one will be successful. After the third round, roughly 83.3% of the survivors of round two will be successful. And on it goes… After twenty rounds, there will be a small handful of extremely successful and wealthy Russian roulette players. However, these cases of extreme success are due entirely to luck.

In the business world, of course, there are many cases where skill plays a large role. The point is that our brains by nature are unable to see when luck has played a role in some successful outcome. And luck almost always plays an important role in most areas of life.

Taleb points out that there are some areas where success is due mostly to skill and not luck. Taleb likes to give the example of dentistry. The success of a dentist will typically be due mostly to skill.

Taleb attributes some of his attitude towards risk to the fact that at one point he had a boss who forced him to consider every possible scenario, no matter how remote.

Interestingly, Taleb understands Homer’sThe Iliad as presenting the following idea: heroes are heroes based on heroic behavior and not based on whether they won or lost. Homer seems to have understood the role of chance (luck).

THREE: A MATHEMATICAL MEDITATION ON HISTORY

A Monte Carlo generator creates manyalternative random sample paths. Note that a sample path can be deterministic, but our concern here is with random sample paths. Also note that some random sample paths can have higher probabilities than other random sample paths. Each sample path represents just one sequence of events out of many possible sequences, ergo the word “sample”.

Taleb offers a few examples of random sample paths. Consider the price of your favorite technology stock, he says. It may start at $100, hit $220 along the way, and end up at $20. Or it may start at $100 and reach $145, but only after touching $10. Another example might be your wealth during at a night at the casino. Say you begin with $1,000 in your pocket. One possibility is that you end up with $2,200, while another possibility is that you end up with only $20.

Photo by Emily2k

Taleb says:

My Monte Carlo engine took me on a few interesting adventures. While my colleagues were immersed in news stories, central bank announcements, earnings reports, economic forecasts, sports results and, not least, office politics, I started toying with it in fields bordering my home base of financial probability. A natural field of expansion for the amateur is evolutionary biology… I started simulating populations of fast mutating animals called Zorglubs under climactic changes and witnessing the most unexpected of conclusions… My aim, as a pure amateur fleeing the boredom of business life, was merely to develop intuitions for these events… I also toyed with molecular biology, generating randomly occurring cancer cells and witnessing some surprising aspects to their evolution.

Taleb continues:

Naturally the analogue to fabricating populations of Zorglubs was to simulate a population of “idiotic bull”, “impetuous bear”, and “cautious” traders under different market regimes, say booms and busts, and to examine their short-term and long-term survival… My models showed almost nobody to really ultimately make money; bears dropped out like flies in the rally and bulls got ultimately slaughtered, as paper profits vanished when the music stopped. But there was one exception; some of those who traded options (I called them option buyers) had remarkable staying power and I wanted to be one of those. How? Because they could buy insurance against the blowup; they could get anxiety-free sleep at night, thanks to the knowledge that if their careers were threatened, it would not be owing to the outcome of a single day.

Note from a value investing point of view

A value investor seeks to pay low prices for stock in individual businesses. Stock prices can jump around in the short term. But over time, if the business you invest in succeeds, then the stock will follow, assuming you bought the stock at relatively low prices. Again, if there’s a bear market or a market crash, and if the stock prices of the businesses in which you’ve invested decline, then that presents a wonderful opportunity to buy more stock at attractively low prices. Over time, the U.S. and global economy will grow, regardless of the occasional market panic or crash. Because of this growth, one of the lowest risk ways to build wealth is to invest in businesses, either on an individual basis if you’re a value investor or via index funds.

Taleb’s methods of trying to make money during a market panic or crash will almost certainly doless well over the long term than simple index funds.

Taleb makes a further point: The vast majority of people learn only from their own mistakes, and rarely from the mistakes of others. Children only learn that the stove is hot by getting burned. Adults are largely the same way: We only learn from our own mistakes. Rarely do we learn from the mistakes of others. And rarely do we heed the warnings of others. Taleb:

All of my colleagues whom I have known to denigrate history blew up spectacularly–and I have yet to encounter some such person who has not blown up.

Keep in mind that Taleb is talking about traders here. For a regular investor who dollar cost averages into index funds and/or who uses value investing, Taleb’s warning does not apply. As a long-term investor in index funds and/or in value investing techniques, you do have to be ready for a 50% decline at some point. But if you buy more after such a decline, your long-term results will actually be helped, not hurt, by a 50% decline.

Taleb points out that aged traders and investors are likely better to use as role models precisely because they have been exposed to markets longer. Taleb:

I toyed with Monte Carlo simulations of heterogeneous populations of traders under a variety of regimes (closely resembling historical ones), and found a significant advantage in selecting aged traders, using, as a selection criterion their cumulative years of experience rather than their absolute success (conditional on their having survived without blowing up).

Taleb also observes that there is a similar phenomenon in mate selection. All else equal, women prefer to mate with healthy older men over healthy younger ones. Healthy older men, by having survived longer, show some evidence of better genes.

FOUR: RANDOMNESS, NONSENSE, AND THE SCIENTIFIC INTELLECTUAL

Using a random generator of words, it’s possible to create rhetoric, but it’s not possible to generate genuine scientific knowledge.

FIVE: SURVIVAL OF THE LEAST FIT–CAN EVOLUTION BE FOOLED BY RANDOMNESS?

Taleb writes about Carlos “the emerging markets wizard.” After excelling as an undergraduate, Carlos went for a PhD. in economics from Harvard. Unable to find a decent thesis topic for his dissertation, he settled for a master’s degree and a career on Wall Street.

Carlos did well investing in emerging markets bonds. One important reason for his success, beyond the fact that he bought emerging markets bonds that later went up in value, was that he bought the dips. Whenever there was a momentary panic and emerging markets bonds dropped in value, Carlos bought more. This dip buying improved his performance. Taleb:

It was the summer of 1998 that undid Carlos–that last dip did not translate into a rally. His track record today includes just one bad quarter–but bad it was. He had earned close to $80 million cumulatively in his previous years. He lost $300 million in just one summer.

When the market first started dipping, Carlos learned that a New Jersey hedge fund was liquidating, including its position in Russian bonds. So when Russian bonds dropped to $52, Carlos was buying. To those who questioned his buying, he yelled: “Read my lips: it’s li-qui-da-tion!”

Taleb continues:

By the end of June, his trading revenues for 1998 had dropped from up $60 million to up $20 million. That made him angry. But he calculated that should the market rise back to the pre-New Jersey selloff, then he would be up $100 million. That was unavoidable, he asserted. These bonds, he said, would never, ever trade below $48. He was risking so little, to possibly make so much.

Then came July. The market dropped a bit more. The benchmark Russian bond was now $43. His positions were under water, but he increased his stakes. By now he was down $30 million for the year. His bosses were starting to become nervous, but he kept telling them that, after all, Russia would not go under. He repeated the cliche that it was too big to fail. He estimated that bailing them out would cost so little and would benefit the world economy so much that it did not make sense to liquidate his inventory now.

Carlos asserted that the Russian bonds were trading near default value. If Russia were to default, then Russian bonds would stay at the same prices they were at currently. Carlos took the further step of investing half of his net worth, then $5,000,000, into Russian bonds.

Russian bond prices then dropped into the 30s, and then into the 20s. Since Carlos thought the bonds could not be less than the default values he had calculated, and were probably worth much more, he was not alarmed. He maintained that anyone who invested in Russian bonds at these levels would realize wonderful returns. He claimed that stop losses “are for schmucks! I am not going to buy high and sell low!” He pointed out that in October 1997 they were way down, but that buying the dip ended up yielding excellent profits for 1997. Furthermore, Carlos pointed out that other banks were showing even larger losses on their Russian bond positions. Taleb:

Towards the end of August, the bellwether Russian Principal Bonds were trading below $10. Carlos’s net worth was reduced by almost half. He was dismissed. So was his boss, the head of trading. The president of the bank was demoted to a “newly created position”. Board members could not understand why the bank had so much exposure to a government that was not paying its own employees–which, disturbingly, included armed soldiers. This was one of the small points that emerging market economists around the globe, from talking to each other so much, forgot to take into account.

Taleb adds:

Louie, a veteran trader on the neighboring desk who suffered much humiliation by these rich emerging market traders, was there, vindicated. Louie was then a 52-year-old Brooklyn-born-and-raised trader who over three decades survived every single conceivable market cycle.

Taleb concludes that Carlos is a gentleman, but a bad trader:

He has all of the traits of a thoughtful gentleman, and would be an ideal son-in-law. But he has most of the attributes of the bad trader. And, at any point in time, the richest traders are often the worst traders. This, I will call thecross-sectional problem: at a given time in the market, the most profitable traders are likely to be those that are best fit to the latest cycle.

Taleb discusses John the high-yield trader, who was mentioned near the beginning of the book, as another bad trader. What traits do bad traders, who may be lucky idiots for awhile, share? Taleb:

An overestimation of the accuracy of their beliefs in some measure, either economic (Carlos) or statistical (John). They don’t consider that what they view as economic or statistical truth may have been fit to past events and may no longer be true.

A tendency to get married to positions.

The tendency to change their story.

No precise game plan ahead of time as to what to do in the event of losses.

Absence of critical thinking expressed in absence of revision of their stance with “stop losses”.

Denial.

SIX: SKEWNESS AND ASYMMETRY

Taleb presents the following Table:

Event

Probability

Outcome

Expectation

A

999/1000

$1

$.999

B

1/1000

-$10,000

-$10.00

Total

-$9.001

The point is that thefrequency of losing cannot be considered apart from themagnitude of the outcome. If you play the game, you’re extremely likely to make $1. But it’s not a good idea to play. If you play this game millions of times, you’re virtually guaranteed to lose money.

Taleb comments that even professional investors misunderstand this bet:

How could people miss such a point? Why do they confuse probability and expectation, that is, probability and probability times the payoff? Mainly because much of people’s schooling comes from examples in symmetric environments, like a coin-toss, where such a difference does not matter. In fact the so-called “Bell Curve” that seems to have found universal use in society is entirely symmetric.

(Coin toss. Photo by Christian Delbert)

Taleb gives an example where he is shorting the S&P 500 Index. He thought the market had a 70% chance of going up and a 30% chance of going down. But he thought that if the market went down, it could go down a lot. Therefore, it was profitable over time (by repeating the bet) to be short the S&P 500.

Note: From a value investing point of view, no one can predict what the market will do. But you can predict what some individual businesses are likely to do. The key is to invest in businesses when the price (stock) is low.

Rare Events

Taleb explains his trading strategy:

The best description of my lifelong business in the market is “skewed bets”, that is, I try to benefit from rare events, events that do not tend to repeat themselves frequently, but, accordingly, present a large payoff when they occur. I try to make money infrequently, as infrequently as possible, simply because I believe that rare events are not fairly valued, and that the rarer the event, the more undervalued it will be in price.

Illustration by lqoncept

Taleb gives an example where his strategy paid off:

One such rare event is the stock market crash of 1987, which made me as a trader and allowed me the luxury of becoming involved in all manner of scholarship.

Taleb notes that in most areas of science, it is common practice to discardoutliers when computing the average. For instance, a professor calculating the average grade in his or her class might discard the highest and the lowest values. In finance, however, it is often wrong to discard the extreme outcomes because, as Taleb has shown, the magnitude of an extreme outcome can matter.

Taleb advises studying market history. But then again, you have to be careful, as Taleb explains:

Sometimes market data becomes a simple trap; it shows you the opposite of its nature, simply to get you to invest in the security or mismanage your risks. Currencies that exhibit the largest historical stability, for example, are the most prone to crashes…

Taleb notes the following:

In other words history teaches us that things that never happened before do happen.

History does not always repeat. Sometimes things change. For instance, today the U.S. stock market seems high. The S&P 500 Index is over 3,000. Based on history, one might expect a bear market and/or a recession. There hasn’t been a recession in the U.S. since 2009.

However, with interest rates low, and with the profit margins on many technology companies high, it’s possible that stocks will not decline much, even if there’s a recession. It’s also possible that any recession could be delayed, partly because the Fed and other central banks remain very accommodative. It’s possible that the business cycle itself may be less volatile because the fiscal and monetary authorities have gotten better at delaying recessions or at making recessions shallower than before.

Ironically, to the extent that Taleb seeks to profit from a market panic or crash, for the reasons just mentioned, Taleb’s strategy may not work as well going forward.

Taleb introducesthe problem of stationarity. To illustrate the problem, think of an urn with red balls and black balls in it. Taleb:

Think of an urn that is hollow at the bottom. As I am sampling from it, and without my being aware of it, some mischievous child is adding balls of one color or another. My inference thus becomes insignificant. I may infer that the red balls represent 50% of the urn while the mischievous child, hearing me, would swiftly replace all the red balls with black ones. This makes much of our knowledge derived through statistics quite shaky.

The very same effect takes place in the market. We take past history as a single homogeneous sample and believe that we have considerably increased our knowledge of the future from the observation of the sample of the past. What if vicious children were changing the composition of the urn? In other words, what if things have changed?

Taleb notes that there are many techniques that use past history in order to measure risks going forward. But to the extent that past data are not stationary, depending upon these risk measurement techniques can be a serious mistake. All of this leads to a more fundamental issue: the problem of induction.

SEVEN: THE PROBLEM OF INDUCTION

Taleb quotes the Scottish philosopher David Hume:

No amount of observations of white swans can allow the inference that all swans are white, but the observation of a single black swan is sufficient to refute that conclusion.

(Black swan. Photo by Damithri)

Taleb came to believe that Sir Karl Popper had an important answer to the problem of induction. According to Popper, there are only two types of scientific theories:

Theories that are known to be wrong, as they were tested and adequately rejected (i.e., falsified).

Theories that have not yet been known to be wrong, not falsified yet, but are exposed to be proved wrong.

It also follows that we should not always rely on statistics. Taleb:

More practically to me, Popper had many problems with statistics and statisticians. He refused to blindly accept the notion that knowledge can always increase with incremental information–which is the foundation for statistical inference. It may in some instances, but we do not know which ones. Many insightful people, such as John Maynard Keynes, independently reached the same conclusions. Sir Karl’s detractors believe that favorably repeating the same experiment again and again should lead to an increased comfort with the notion that “it works”.

Taleb explains the concept of anopen society:

Popper’s falsificationism is intimately connected to the notion of an open society. An open society is one in which no permanent truth is held to exist; this would allow counterideas to emerge.

For Taleb, a successful trader or investor must have anopen mind in which no permanent truth is held to exist.

Taleb concludes the chapter by applying the logic of Pascal’s wager to trading and investing:

…I will use statistics and inductive methods to make aggressive bets, but I will not use them to manage my risks and exposure. Surprisingly, all the surviving traders I know seem to have done the same. They trade on ideas based on some observation (that includes past history) but, like the Popperian scientists, they make sure that the costs of being wrong are limited (and their probability is not derived from past data). Unlike Carlos and John, they know before getting involved in the trading strategy which events would prove their conjecture wrong and allow for it (recall the Carlos and John used past history both to make their bets and measure their risk).

PART II: MONKEYS ON TYPEWRITERS–SURVIVORSHIP AND OTHER BIASES

If you put an infinite number of monkeys in front of typewriters, it is certain that one of them will type an exact version of Homer’s The Iliad. Taleb asks:

Now that we have found that hero among monkeys, would any reader invest his life’s savings on a bet that the monkey would writeThe Odyssey next?

Infinite number of monkeys on typewriters. Illustration by Robert Adrian Hillman.

EIGHT: TOO MANY MILLIONAIRES NEXT DOOR

Taleb begins the chapter by describing a lawyer named Marc. Marc makes $500,000 a year. He attended Harvard as an undergraduate and then Yale Law School. The problem is that some of Marc’s neighbors are much wealthier. Taleb discusses Marc’s wife, Janet:

Every month or so, Janet has a crisis… Why isn’t her husband so successful? Isn’t he smart and hard working? Didn’t he get close to 1600 on the SAT? Why is Ronald Something whose wife never even nods to Janet worth hundred of millions when her husband went to Harvard and Yale and has such a high I.Q., and has hardly any substantial savings?

Note: Warren Buffett and Charlie Munger have long made the point that envy is a massively stupid sin because, unlike other sins (e.g., gluttony), you can’t have any fun with it. Granted, envy is a very human emotion. But we can and must train ourselves not to fall into it.

Daniel Kahneman and others have demonstrated that the average person would rather make $70,000 as long as his neighbor makes $60,000 than make $80,000 if his neighbor makes $90,000. How stupid to compare ourselves to people who happen to be doing better! There will always be someone doing better.

Taleb mentions the book,The Millionaire Next Door. One idea from the book is that the wealthy often do not look wealthy because they’re focused on saving and investing, rather than on spending. However, Taleb finds two problems with the book. First, the book does not adjust for survivorship bias. In other words, for at least some of the wealthy, there is some luck involved. Second, there’s the problem of induction. If you measure someone’s wealth in the year 2000 (Taleb was writing in 2001), at the end of one of the biggest bull markets in modern history (from 1982 to 2000), then in many cases a large degree of that wealth came as a result of the prolonged bull market. By contrast, if you measure people’s wealth in 1982, there would be fewer people who are millionaires, even after adjusting for inflation.

NINE: IT IS EASIER TO BUY AND SELL THAN FRY AN EGG

Taleb writes about going to the dentist and being confident that his dentist knows something about teeth. Later, Taleb goes to Carnegie Hall. Before the pianist begins her performance, Taleb has zero doubt that she knows how to play the piano and is not about to produce cacophony. Later still, Taleb is in London and ends up looking at some of his favorite marble statues. Once again, he knows they weren’t produced by luck.

However, in many areas of business and even more so when it comes to investing, luck does tend to play a large role. Taleb is supposed to meet with a fund manager who has a good track record and who is looking for investors. Taleb comments that buying and selling, which is what the fund manager does, is easier than frying an egg. The problem is that luck plays such a large role in almost any good investment track record.

Photo by Alhovik

In order to study the role luck plays for investors, Taleb suggests a hypothetical game. There are 10,000 investors at the beginning. In the first round, a fair coin is tossed for each investor. Heads, and the investor makes $10,000, tails, and the investor loses $10,000. (Any investor who has a losing year is not allowed to continue to play the game.) After the first round, there will be about 5,000 successful investors. In the second round, a fair coin is again tossed. After the second round, there will be 2,500 successful investors. Another round, and 1,250 will remain. A fourth round, and 625 successful investors will remain. A fifth round, and 313 successful investors will remain. Based on luck alone, after five years there will be approximately 313 investors with winning track records. No doubt these 313 winners will be puffed up with serotonin.

Taleb then observes that you can play the same hypothetical game with bad investors. You assume each year that there’s a 45% chance of winning and a 55% chance of losing. After one year, 4,500 successful (but bad) investors will remain. After two years, 2,025. After three years, 911. After four years, 410. After five years, there will be 184 bad investors who have successful track records.

Taleb makes two counterintuitive points:

First, even starting with only bad investors, you will end up with a small number of great track records.

Second, how many great track records you end up with depends more on the size of the initial sample–how many investors you started with–than it does on the individual odds per investor. Applied to the real world, this means that if there are more investors who start in 1997 than in 1993, then you will see a greater number of successful track records in 2002 than you will see in 1998.

Taleb concludes:

Recall that the survivorship bias depends on the size of the initial population. The information that a person made money in the past, just by itself, is neither meaningful nor relevant. We need to know that size of the population from which he came. In other words, without knowing how many managers out there have tried and failed, we will not be able to assess the validity of the track record. If the initial population includes ten managers, then I would give the performer half my savings without a blink. If the initial population is composed of 10,000 managers, I would ignore the results.

The mysterious letter

Taleb tells a story. You get a letter on Jan. 2 informing you that the market will go up during the month. It does. Then you get a letter on Feb. 1 saying the market will go down during the month. It does. You get another letter on Mar. 1. Same story. Again for April and for May. You’ve now gotten five letters in a row predicting what the market would do during the ensuing month, and all five letters were correct. Next you are asked to invest in a special fund. The fund blows up. What happened?

The trick is as follows. The con operator gets 10,000 random names. On Jan. 2, he mails 5,000 letters predicting that the market will go up and 5,000 letters predicting that the market will go down. The next month, he focuses only on the 5,000 names who were just mailed a correct prediction. He sends 2,500 letters predicting that the market will go up and 2,500 letters predicting that the market will go down. Of course, next he focuses on the 2,500 letters which gave correct predictions. He mails 1,250 letters predicting a market rise and 1,250 predicting a market fall. After five months of this, there will be approximately 200 people who received five straight correct predictions.

Taleb suggests the birthday paradox as an intuitive way to explain the data mining problem. If you encounter a random person, there is a one in 365.25 chance that you have the same birthday. But if you have 23 random people in a room, the odds are close to 50 percent that you can find two people who share a birthday.

Similarly, what are the odds that you’ll run into someone you know in a totally random place? The odds are quite high because you are testing for any encounter, with any person you know, in any place you will visit.

Taleb continues:

What is your probability of winning the New Jersey lottery twice? One in 17 trillion. Yet it happened to Evelyn Adams, whom the reader might guess should feel particularly chosen by destiny. Using the method we developed above, Harvard’s Percy Diaconis and Frederick Mosteller estimated at 30 to 1 the probability the someone, somewhere, in a totally unspecified way, gets so lucky!

What isdata snooping? It’s looking at historical data to determine the hypothetical performance of a large number of trading rules. The more trading rules you examine, the more likely you are to find trading rules that would have worked in the past and that one might expect to work in the future. However, many such trading rules would have worked in the past based on luck alone.

Taleb next writes about companies that increase their earnings. The same logic can be applied. If you start out with 10,000 companies, then by luck 5,000 will increase their profits after the first year. After three years, there will be 1,250 “stars” that increased their profits for three years in a row. Analysts will rate these companies a “strong buy”. The point is not that profit increases are entirely due to luck. The point, rather, is that luck often plays a significant role in business results, usually far more than is commonly supposed.

TEN: LOSER TAKES ALL–ONE THE NONLINEARITIES OF LIFE

Taleb writes:

This chapter is about how a small advantage in life can translate into a highly disproportionate payoff, or, more viciously, how no advantage at all, but a very, very small help from randomness, can lead to a bonanza.

Nonlinearity is when a small input can lead to a disproportionate response. Consider a sandpile. You can add many grains of sand with nothing happening. Then suddenly one grain of sand causes an avalanche.

(Photo by Maocheng)

Taleb mentions actors auditioning for parts. A handful of actors get certain parts, and a few of them become famous. The most famous actors are not always the best actors (although they often are). Rather, there could have been random (lucky) reasons why a handful of actors got certain parts and why a few of them became famous.

The QWERTY keyboard is not optimal. But so many people were trained on it, and so many QWERTY keyboards were manufactured, that it has come to dominate. This is called a path dependent outcome. Taleb comments:

Such ideas go against classical economic models, in which results either come from a precise reason (there is no account for uncertainty) or the good guy wins (the good guy is the one who is more skilled and has some technical superiority)… Brian Arthur, an economist concerned with nonlinearities at the Santa Fe Institute, wrote that chance events coupled with positive feedback rather than technological superiority will determine economic superiority–not some abstrusely defined edge in a given area of expertise. While early economic models excluded randomness, Arthur explained how “unexpected orders, chance meetings with lawyers, managerial whims… would help determine which ones achieved early sales and, over time, which firms dominated”.

Taleb continues by noting that Arthur suggests a mathematical model called the Polya process:

The Polya process can be presented as follows: assume an urn initially containing equal quantities of black and red balls. You are to guess each time which color you will pull out before you make the draw. Here the game is rigged. Unlike a conventional urn, the probability of guessing correctly depends on past success, as you get better or worse at guessing depending on past performance. Thus the probability of winning increases after past wins, that of losing increases after past losses. Simulating such a process, one can see a huge variance of outcomes, with astonishing successes and a large number of failures (what we called skewness).

ELEVEN: RANDOMNESS AND OUR BRAIN–WE ARE PROBABILITY BLIND

Our genes have not yet evolved to the point where our brains can naturally compute probabilities. Computing probabilities is not something we even needed to do until very recently.

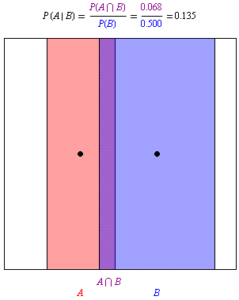

Here’s a diagram of how to compute the probability of A, conditional on B having happened:

(Diagram by Oleg Alexandrov, via Wikimedia Commons)

Taleb:

We are capable of sending a spacecraft to Mars, but we are incapable of having criminal trials managed by the basic laws of probability–yet evidence is clearly a probabilistic notion…

People who are as close to being criminal as probability laws can allow us to infer (that is with a confidence that exceeds theshadow of a doubt) are walking free because of our misunderstanding of basic concepts of the odds… I was in a dealing room with a TV set turned on when I saw one of the lawyers arguing that there were at least four people in Los Angeles capable of carrying O.J. Simpson’s DNA characteristics (thus ignoring the joint set of events…). I then switched off the television set in disgust, causing an uproar among the traders. I was under the impression until then that sophistry had been eliminated from legal cases thanks to the high standards of republican Rome. Worse, one Harvard lawyer used the specious argument that only 10% of men who brutalize their wives go on to murder them, which is a probability unconditional on the murder… Isn’t the law devoted to the truth? The correct way to look at it is to determine the percentage of murder cases where women were killed by their husbandand had previously been battered by him (that is, 50%)–for we are dealing with what is called conditional probabilities; the probability that O.J. killed his wifeconditional on the information of her having been killed, rather than theunconditional probability of O.J. killing his wife. How can we expect the untrained person to understand randomness when a Harvard professor who deals and teaches the concept of probabilistic evidence can make such an incorrect statement?

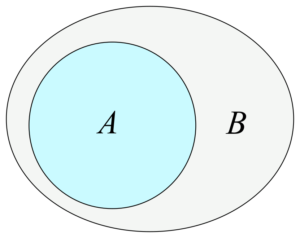

Speaking of people misunderstanding probabilities, Daniel Kahneman and Amos Tversky have asked groups to answer the following question:

Linda is 31 years old, single, outspoken, and very bright. She majored in philosophy. As a student, she was deeply concerned with issues of discrimination and social justice, and also participated in anti-nuclear demonstrations.

Which is more probable?

Linda is a bank teller.

Linda is a bank teller and is active in the feminist movement.

The majority of people believe that 2. is more probable the 1. But that’s an obvious fallacy. Bank tellers who are also feminists is a subset of all bank tellers, therefore 1. is more probable than 2. To see why, consider the following diagram:

(By svjo, via Wikimedia Commons)

B represents ALL bank tellers. Out of ALL bank tellers, some are feminists and some are not. Those bank tellers that are also feminists is represented by A.

Here’s a probability question that was presented to doctors:

A test of a disease presents a rate of 5% false positives. The disease strikes 1/1,000 of the population. People are tested at random, regardless of whether they are suspected of having the disease. A patient’s test is positive. What is the probability of the patient being stricken with the disease?

Many doctors answer 95%, which is wildly incorrect. The answer is close to 2%. Less than one in five doctors get the question right.

To see the right answer, assume that there are no false negatives. Out of 1,000 patients, one will have the disease. Consider the remaining 999. 50 of them will test positive. The probability of being afflicted with the disease for someone selected at random who tested positive is the following ratio:

Number of afflicted persons / Number of true and false positives

So the answer is 1/51, about 2%.

Another example where people misunderstand probabilities is when it comes to valuing options. (Recall that Taleb is an options trader.) Taleb gives an example. Say that the stock price is $100 today. You can buy a call option for $1 that gives you the right to buy the stock at $110 any time during the next month. Note that the option is out-of-the-money because you would not gain if you exercised your right to buy now, given that the stock is $100, below the exercise price of $110.

Now, what is the expected value of the option? About 90 percent of out-of-the-money options expire worthless, that is, they end up being worth $0. But the expected value is not $0 because there is a 10 percent chance that the option could be worth, say $10, because the stock went to $120. So even though it is 90 percent likely that the option will end up being worth $0, the expected value is not $0. The actual expected value in this example is:

(90% x $0) + (10% x $10) = $0 + $1 = $1

The expected value of the option is $1, which means you would have paid a fair price if you had bought it for $1. Taleb notes:

I discovered very few people who accepted losing $1 for most expirations and making $10 once in a while, even if the game were fair (i.e., they made the $10 more than 10% of the time).

“Fair” is not the right term here. If you make $10 more than 10% of the time, then the game has apositive expected value. That means if you play the game repeatedly, then eventually over time you will make money. Taleb’s point is that even if the game has a positive expected value, very few people would like to play it because on your way to making money, you have to accept small losses most of the time.

Taleb distinguishes betweenpremium sellers, who sell options, andpremium buyers, who buy options. Following the same logic as above, premium sellers make small amounts of money roughly 90% of the time, and then take a big loss roughly 10% of the time. Premium buyers lose small amounts about 90% of the time, and then have a big gain about 10% of the time.

Is it better to be an option seller or an option buyer? It depends on whether you can find favorable odds. It also depends on your temperament. Most people do not like taking small losses most of the time. Taleb:

Alas, most option traders I encountered in my career arepremium sellers–when they blow up it is generally other people’s money.

PART III: WAX IN MY EARS–LIVING WITH RANDOMITIS