Would you like to improve as an investor? One of the best things you can do is to study great investors like Warren Buffett.

Robert Hagstrom has written an excellent book–The Warren Buffett Way(Wiley, 2014)–explaining Buffett’s approach to investing. Hagstrom’s goal is to help investors improve.

Here is the outline for this blog post:

- A Five-Sigma Event: The World’s Greatest Investor

- The Education of Warren Buffett

- Buying a Business: The Twelve Immutable Tenets

- Common Stock Purchases: Nine Case Studies

- Portfolio Management: The Mathematics of Investing

- The Psychology of Investing

- The Value of Patience

- The World’s Greatest Investor

(Photo by USA International Trade Administration)

A FIVE-SIGMA EVENT: THE WORLD’S GREATEST INVESTOR

Buffett has always maintained that he won the ovarian lottery.

My wealth has come from a combination of living in America, some lucky genes, and compound interest. My luck was accentuated by my living in a market system that sometimes produces distorted results, though overall it serves our country well.

Buffett keeps things in perspective by saying that he happens to work “in an economy that rewards someone who saves lives of others on a battlefield with a medal, rewards a great teacher with thank-you notes from parents, but rewards those who can detect mispricing of securities with sums reaching into the billions.”

Buffett was entrepreneurial from a young age. He would buy a six-pack of coke for 25 cents, then sell each one for 6 cents. He had two paper routes during the time he lived in Washington, D.C., when his father was a congressman from Nebraska. He and a buddy bought used pinball machines, and made a profit from them.

(Photo by Shahroozporia, via Wikimedia Commons)

But Buffett didn’t figure out the right way to invest for some time. He tried charting. He read books on technical analysis. He got hot tips from brokers. Finally, he came across a copy of The Intelligent Investor, by Benjamin Graham. Buffett then realized that the strategy of value investing explained by Graham was a reliable way to succeed at investing over time.

Buffett attendedgraduate school at Columbia University in order to study under Graham. Once in Graham’s class, everyone saw that Buffett was the brightest and most knowledgeable student. The class was like a conversation between Graham and Buffett. Buffett got an A+ in the course, the first A+ Graham had given in 22 years of teaching.

Upon graduating from Columbia, Buffett was not able to work for Graham at Graham-Newman right away. At the time, Graham was only hiring Jewish analysts because they were being discriminated against elsewhere. Buffett periodically sent Graham stock ideas until Graham finally hired him.

Two years later in 1956, after Graham retired, Buffett returned to Omaha. Buffett launched a limited investment partnership, which included some family and friends as investors. At the outset, the partnership had $105,000 under management.

Buffett’s goal was to beat the Dow Jones Industrial Average by 10 percentage points a year. Approximately thirteen years later, Buffett had beaten the Dow Jones Average by over 22 percentage points a year.

In the early 1960s there was a corporate scandal. The Allied Crude Vegetable Oil Company, led by Tino De Angelis, found that it could get loans based on its inventory of salad oil. De Angelis built a refinery in New Jersey with 139 five-story storage tanks. Because oil floats on top of water, De Angelis filled the tanks with water with just a few feet of oil on the top. The inspectors didn’t notice for some time.

American Express lost $58 million in the salad oil scandal, and its stock dropped over 50 percent. Buffett went to restaurants in Omaha, and discovered that there was no decrease in usage of the American Express Green Card. Buffett also visited banks and learned that the scandal was having no impact on the use of American Express Travelers Cheques.

(Amex Logo, by American Express via Wikimedia Commons)

The strong brand of American Express was still intact. The stock had plummeted based on a huge, but temporary problem. So Buffett invested 40 percent of the partnership in American Express. The shares nearly tripled over the next two years.

By 1965, Buffett had acquired–via the partnership–a controlling interest in Berkshire Hathaway, a struggling New England textile company. When Buffett closed his investment partnership in 1969, he himself kept his stock in Berkshire Hathaway and limited partners received some stock in Berkshire Hathaway. Buffett advised limited partners on how to invest in municipal bonds. (Buffett thought that stocks were not a very good value in 1969.) Or limited partners could invest with Bill Ruane, Buffett’s friend from Columbia University and Graham-Newman. Meanwhile, Berkshire Hathaway, despite excellent management from Ken Chace, had disappointing results for many years. Buffett only kept Berkshire Hathaway open out of concern for the workers.

The textile mills were the largest employer in the area; the workforce was an older age group that possessed relatively nontransferable skills; management had shown a high degree of enthusiasm; the unions were being reasonable; and, very importantly, Buffett believed that some profits could be realized from the textile business.

But Berkshire Hathaway continued to struggle. Buffett siphoned off cash from the business in order to invest in better businesses. (Had the cash been reinvested in Berkshire, the returns would have been below the cost of capital, thus destroying value.) Later, Buffett reluctantly closed Berkshire Hathaway because unending losses would otherwise have been the result.

(Hathaway Mills, Photo byMarcbela via Wikimedia Commons)

In 1967, with the excess cash from the textile operations, Berkshire Hathaway purchased two insurance companies headquartered in Omaha: National Indemnity Company and National Fire & Marine Insurance Company. As Hagstrom writes, this was the beginning of Berkshire Hathaway’s legendary success story.

Instead of having the float from the insurance operations invested mostly in bonds, Buffett invested much of the float in stocks. Over time, due to Buffett’s great skill in investing, investment assets grew significantly in value. Importantly, the underlying insurance operations themselves were profitable because they were disciplined in pricing their policies. The profitability of the insurance operations meant that the float had a very low cost.

Going forward, Buffett was open to investing in more insurance companies. By 1991, Berkshire owned nearly half of GEICO. GEICO was a very profitable auto insurer. GEICO had structurally lower costs than its competitors because GEICO sold direct to customers, without needing agents or branch offices.

Buffett bought other insurance companies over time, including large reinsurers. Hagstrom notes that Buffett’s best acquisition was a person–Ajit Jain. Jain has brilliantly managed the Berkshire Hathaway Reinsurance Group over the years. Buffett said of Ajit:

His operation combines capacity, speed, decisiveness, and most importantly, brains in a manager that is unique in the insurance business.

Over several decades, Buffett invested in a focused portfolio of common stocks. He also acquired a number of private businesses. He views both types of investment the same way: he looks to pay a good price for a simple business, run by able and honest management, with good economics.

Hagstrom notes Buffett’s track record:

Over the past 48 years, starting in 1965, the year Buffett took control of Berkshire Hathaway, the book value of the company has grown from $19 to $114,214 per share, a compounded gain of 19.7 percent; during that period, the Standard & Poor’s (S&P) 500 index gained 9.4 percent, dividends included.

The margin of outperformance combined with the length of the track record is simply unparalleled in the investment world. But Hagstrom argues that other investors can improve by studying Buffett’s career. Hagstrom quotes Buffett:

What we do is not beyond anyone else’s competence. I feel the same way about managing that I do about investing: it is just not necessary to do extraordinary things to get extraordinary results.

THE EDUCATION OF WARREN BUFFETT

Hagstrom writes that Buffett was influenced primarily by three investors: Benjamin Graham, Philip Fisher, and Charlie Munger.

At age 20, Graham graduated from Columbia University and was offered several positions at the university (in literature, mathematics, and philosophy). Graham was clearly a genius. Perhaps based partly on his experience of poverty–his father had died while Graham was young, leaving the family in a difficult financial situation–Graham decided to work on Wall Street rather than work in academia.

Graham’s first job was as a messenger–for $12 a week–for the brokerage firm of Newburger, Henderson & Loeb. Five years later, in 1919, Graham was earning $600,000 a year (almost $8 million in 2012 dollars) as a partner in the firm.

Graham launched Graham-Newman in 1926. In 1929-1932, Graham-Newman lost most of its value. Graham personally was financially ruined.

From 1929 to 1934, Graham, while teaching at Columbia University and in cooperation with another professor, David Dodd, produced Security Analysis, which continues to be the bible for value investors to this day. Graham was slowly rebuilding his fortune, and the philosophy of value investing–as expressed in Security Analysis–was the key.

(Ben Graham, by Equim43 via Wikimedia Commons)

Graham realized that many investors try to get good results over short periods of time. He saw that short-term movements in stock prices are largely random and unpredictable, but that over time, a stock price follows the earnings of a company. Graham thus distinguished between speculation and investing. Speculation meant trying to predict stock prices over the short term, whereas investing means buying below probable intrinsic value–based on net asset value or earnings power.

Intrinsic value is based on net asset value or earnings power. As long as the investor pays a price below intrinsic value, the investor has a margin of safety. The margin of safety offers protection against errors by the investor and against bad luck (or unforeseen negative events). Simultaneously, the margin of safety represents the profit the investor can earn in those cases where he or she is right and the stock price approaches intrinsic value.

Graham preferred to focus on net asset value. If you take the current assets of the company and subtract all liabilities, and if the stock price can be bought below that level, there is a strong margin of safety present. This is Graham’s net-net approach. It is meant to be applied to a basket of stocks.

The net-net approach is inherently safer than buying stocks at a discount to their earnings power. It is generally more difficult to estimate the earnings power of a company than to estimate the net-net value. (The net-net value is simply an extremely conservative measure of liquidation value.)

Thus Graham placed much more emphasis on quantitative cheapness than he did on qualitative factors like competitive position and management capability. If you keep buying stocks at a huge discount to net asset value, you are nearly certain to get good results over time. On the other hand, if you keep buying stocks at a discount to earnings power, you cannot be as certain because in many cases future earnings may turn out to be different than expected.

In brief, Graham offered two methods for investors to succeed: buying below net current asset value and buying at a low price-to-earnings ratios (P/E). In either case, the stock in question is deeply out of favor.

Every business, at any given time, is either in one of two states: it is experiencing problems or it will be experiencing problems. When a business runs into problems, the stock price typically will decline and the company will fall out of favor. The key is that most business problems are temporary and not permanent, at least when viewed over the subsequent 3 to 5 years.

When a company runs into problems, investors usually overreact and sell the stock to much lower levels than is justified by net asset value or earnings power. By systematically buying a basket of these oversold stocks, you can do well over time.

Philip Fisher

Fisher believed in a concentrated portfolio of five to eight stocks. Fisher would conduct ‘scuttlebutt’ research, which involved speaking with customers, suppliers, competitors, and industry experts. Fisher wanted to understand the quality of management and the strength of the company’s competitive position.

(Philip A. Fisher)

If you can buy stock in a company that has a strong competitive position based on continued innovation, and that is run by able and honest managers, then you’ll do well over time. Fisher also insisted that the sales force of the company in question be strong. This should be ensured by strong management. As well, Fisher made sure the company had good profits.

Good managers focus on building shareholder value. And they are honest about their mistakes and about the real difficulties being encountered by the business.

Charlie Munger

Charlie Munger was from Omaha, like Buffett. As a kid, Munger had worked for the grocery store run by Warren Buffett’s grandfather.

Munger’s grandfather was a federal judge and his father was a lawyer. Munger became a successful lawyer in Los Angeles after graduating from Harvard Law School.

One of Buffett’s early investors, Dr. Edwin Davis, had decided to invest in the Buffett Partnership because Buffett reminded him of Charlie Munger. A few years later, in 1959, Dr. David arranged a meeting between Buffett and Munger. This was the beginning of an extraordinary partnership.

(Charlie Munger at the 2010 Berkshire Hathaway shareholders meeting. Photo by Nick Webb)

Munger realized that it is better to pay a fair price for a wonderful company than a wonderful price for a fair company. Buffett had recently invested in several statistically cheap companies:

My punishment was an education in the economies of short-line farm implementation manufacturers (Dempster Mill Manufacturing), third-place department stores (Hochschild-Kohn), and New England textile manufacturers (Berkshire Hathaway).

These were three situations of paying a wonderful price for a fair company. Only the investment in Dempster worked, thanks to a turnaround specialist, Harry Bottle, whom Munger had introduced to Buffett. The Dempster investment easily could have failed. Hochschild-Kohn didn’t work. Berkshire Hathaway–the textile manufacturer–eventually went out of business.

Note: Buffett took cash out of the textile business and made a long series of highly successful investments. This was the beginning of Buffett and Munger creating today’s Berkshire Hathaway. The old textile business was closed.

In 1972, Berkshire Hathaway acquired See’s Candies at a large premium to book value. This stock was not at all statistically cheap. But it was a wonderful company at a fair price, which Munger argued made excellent sense.

Over the ensuing decades, See’s Candies produced an extraordinarily high return on invested capital (ROIC) and return on equity (ROE). Thus even though Buffett and Munger paid nearly three times book value, the investment turned out to be a grand slam. Charlie said it was ‘the first time we paid for quality.’

The success of the See’s Candies investment is what made Buffett open to making a large investment in Coca-Cola in the late 1980s. Buffett invested about one billion dollars in Coca-Cola–about a third of Berkshire’s portfolio–even though the P/E and the P/CF were high. The key was that Coca-Cola could develop and maintain a very high ROE (and ROIC).

A Blending of Influences

From Graham, Buffett learned the importance of a margin of safety. Buffett learned that it is important to estimate the intrinsic value of the business, and then pay a price well below that value. Buffett also learned from Graham that stock price fluctuations are largely random and should be ignored except when they create bargains. Thirdly, Buffett learned from Graham the importance of being an independent thinker. As Graham said:

You’re neither right nor wrong because the crowd disagrees with you. You’re right because your data and reasoning are right.

From Fisher, Buffett learned to concentrate his portfolio in his best ideas: it is safer to own a few ideas with which you are thoroughly familiar than to own many ideas without knowing much about them. Buffett also learned from Fisher the value of ‘scuttlebutt’ research, which meant interviewing customers, suppliers, competitors, and industry experts. Finally, Buffett learned that a high-quality company can increase its intrinsic value over a long period of time.

Charlie Munger figured out on his own that it made sense to pay a fair price for a wonderful company. Even paying a large premium to book value, you could still have a significant margin of safety relative to a long future of compounding intrinsic value.

Thus it was primarily Munger’s influence that got Buffett to agree to purchase See’s Candies at a large premium to book value. Munger also became an expert in psychology, which impacted Buffett.

Hagstrom sums up the three influences:

Graham gave Buffett the intellectual basis for investing–the margin of safety–and helped him learn to master his emotions in order to take advantage of market fluctuations. Fisher gave Buffett an updated, workable methodology that enabled him to identify good long-term investments and manage a focused portfolio over time. Charlie helped Buffett appreciate the economic returns that come from buying and owning great businesses. [And] Charlie helped educate Buffett on the psychological missteps that often occur when individuals make financial decisions.

BUYING A BUSINESS: THE TWELVE IMMUTABLE TENETS

Buffett uses the same basic approach whether he is acquiring the business outright or buying a piece of the business via shares of stock. Owning the entire company allows Buffett to control the capital allocation of the business. On the other hand, because the stock market is so large, there are many more opportunities to find bargains among public equities than among private businesses. Hagstrom quotes Buffett:

When investing, we view ourselves as business analysts, not as market analysts, not as macroeconomic analysts, and not even as security analysts.

Thus Buffett acts primarily as a businessperson, whether he is acquiring a company or buying stock.

Hagstrom has distilled Buffett’s investment approach into twelve key tenets:

Business Tenets

- Is the business simple and understandable?

- Does the business have a consistent operating history?

- Does the business have favorable long-term prospects?

Management Tenets

- Is management rational?

- Is management candid with its shareholders?

- Does management resist the institutional imperative?

Financial Tenets

- Focus on return on equity (ROE), not earnings per share (EPS).

- Calculate ‘owner earnings.’

- Look for companies with high profit margins.

- For every dollar retained, make sure the company has created at least one dollar of market value.

Market Tenets

- What is the value of the business?

- Can the business be purchased at a significant discount to its value?

Business Tenets

- Is the business simple and understandable?

- Does the business have a consistent operating history?

- Does the business have favorable long-term prospects?

Buffett holds that most business success stories involve companies doing the same things they have been doing for decades. This often does involve ongoing innovation, but in the context of a business that already has a sustainable competitive advantage.

Investment success is not how much you know, but how well you understand the limits of what you know (and what you can know). Buffett:

Invest in your circle of competence. It’s not how big the circle is that counts; it’s how well you define the parameters.

Buffett is looking for a company with a sustainable competitive advantage demonstrated in a consistent operating history and expected to last well into the future. This doesn’t guarantee success in every case, but it does maximize the probability of success over time.

Buffett looks for great businesses or franchises:

He defines a franchise as a company providing a product or service that is (1) needed or desired, (2) has no close substitute, and (3) is not regulated. These traits allow the company to hold its prices, and occasionally raise them, without the fear of losing market share or unit volume. This pricing flexibility is one of the defining characteristics of a great business; it allows the company to earn above-average returns on capital.

(Image by Marek Uliasz)

Buffett:

The key to investing is determining the competitive advantage of any given company and, above all, the durability of the advantage. The products or services that have wide, sustainable moats around them are the ones that deliver rewards to investors.

Buffett again:

[The] definition of a great company is one that will be great for 25 to 30 years.

Management Tenets

- Is management rational?

- Is management candid with its shareholders?

- Does management resist the institutional imperative?

Buffett looks for honest and able managers whobehave like owners. Such managers understand that their mission is to build business value over time.

Allocating capital in a rational way is central to maximizing the value of the business over time. Particularly for mature companies, which Buffett often prefers based on their predictability, the allocation of excess cash can have a large impact on the value of the business.

The key is to get a return on invested capital (ROIC)–or return on equity (ROE)–that exceeds the cost of capital. (ROE is close to ROIC for companies with low or no debt, which Buffett has always preferred.) If there is no project that promises a sufficiently high return on capital, then the managers should consider buying back stock or paying dividends. Buying back stock only creates value when the stock price is below intrinsic value.

When considering projects that may have a high ROIC (or high ROE), it’s vital that managers are thinking independently.

(Photo by Marijus Auruskevicius)

Similarly, managers should never simply copy what other managers in the same industry are doing. This is a recipe for disaster. But it happens often enough. Buffett and Munger call it the institutional imperative–the lemming-like tendency of managers to imitate the behavior of others, no matter how silly or irrational. Buffett and Munger think the institutional imperative is responsible for several problems:

(1) [The organization] resists any change in its current direction; (2) just as work expands to fill available time, corporate projects or acquisitions will materialize to soak up available funds; (3) any business craving of the leader, however foolish, will quickly be supported by detailed rate-of-return and strategic studies prepared by his troops; and (4) the behavior of peer companies, whether they are expanding, acquiring, setting executive compensation or whatever, will be mindlessly imitated.

Jack Ringwalt was the head of National Indemnity when Berkshire acquired it in 1967. There were times when Ringwalt would simply stop selling insurance altogether if the rates on policies didn’t make sense. Buffett learned this lesson well, both for Berkshire’s many insurance operations and in general.

Management candor is essential. Good managers admit their mistakes and confront their problems rather than hiding behind GAAP (generally accepted accounting principles).

Financial Tenets

- Focus on return on equity (ROE), not earnings per share (EPS).

- Calculate ‘owner earnings.’

- Look for companies with high profit margins.

- For every dollar retained, make sure the company has created at least one dollar of market value.

Buffett does not take yearly results too seriously. He focuses on five-year averages. There is too much randomness in periods shorter than five years.

ROE (or ROIC) is more important than EPS. As noted earlier, a company only creates value over time to the extent that its ROIC exceeds its cost of capital. Often the cost of capital can be understood as the opportunity cost of capital, or the next best investment opportunity with a similar level of risk.

In calculating ROE–or ROIC–Buffett excludes extraordinary items. He seeks to isolate the underlying performance of the business.

The intrinsic value of any business is all future free cash flow (FCF) discounted back to the present. Buffett uses the term owner earnings in place of FCF. It equals net income plus depreciation, depletion, and amortization, and minus capital expenditures. (There may also be adjustments for changes in working capital.)

Buffett’s favorite managers minimize costs just like they breathe. They do it automatically at all times.

Market Tenets

- What is the value of the business?

- Can the business be purchased at a significant discount to its value?

The value of any business is all future FCF discounted back to the present. This definition was first explained by John Burr Williams in The Theory of Investment Value.

Buffett compares valuing a business to valuing a bond. You know the coupon and maturity date for the bond, so you know the future cash flows. Then you discount those future cash flows back to the present using an appropriate discount rate.

Buffett nearly always insists on a ‘coupon-like’ certainty for the future cash flows of a business in which he invests. Therefore, Buffett uses the rate of the long-term U.S. government bond as his discount rate. (If rates are very low, as today, Buffett often uses 6% as the discount rate.)

Hagstrom quotes Buffett:

[Irrespective] of whether a business grows or doesn’t, displays volatility or smoothness in earnings, or carries a high price or low in relation to its current earnings and book value, the investment shown by the discounted-flows-of-cash calculation to be the cheapest is the one that the investor should purchase.

Buffett wrote in the 1981 Berkshire Hathaway Letter to Shareholders:

[We have made mistakes as to:] (1) the management we have elected to join; (2) the future economics of the business; or (3) the price we have paid.We have made plenty of such mistakes–both in the purchase of non-controlling and controlling interests in businesses. Category (2) miscalculations are the most common.

Ben Graham taught that you only buy when there is a margin of safety between the price you pay and the intrinsic value of the business. A margin of safety simultaneously lowers the risk of the investment AND increases the potential return. The notion that lowering your risk can increase your return is directly contrary to what is taught in modern finance, where higher returns always require higher risks.

Buffett has adopted Graham’s view that investing means becoming a part owner of a business. Investing is not trading pieces of paper. Graham:

Investing is most intelligent when it is most businesslike.

Buffett says these are “the nine most important words ever written about investing.” For Buffett, becoming a part owner of a public business by buying stock is no different than becoming a part owner–or full owner–of a private business. Buffett notes:

I am a better investor because I am a businessman, and a better businessman because I am an investor.

COMMON STOCK PURCHASES: NINE CASE STUDIES

The Washington Post Company

Millionaire financier Eugene Meyer bought the Washington Post for $825,000 at an auction held to pay off creditors. Much later, Philip Graham, a brilliant Harvard-educated lawyer, took over management of the paper. Graham had married Meyer’s daughter Katharine. Graham transformed the Washington Post from a single newspaper into a media and communications company.

(Photo by Michael Fleischhacker, via Wikimedia Commons)

After Graham’s tragic suicide, control of the paper passed to Katharine Graham. She learned quickly that she had to make decisions. She made two great decisions: hiring Ben Bradlee as managing editor and then inviting Warren Buffett to become a director. Bradlee persuaded Katharine Graham to publish the Pentagon Papers and to pursue the Watergate investigation. This earned the paper a reputation for award-winning journalism. Meanwhile, Buffett taught Katharine Graham how to run a successful business. (Buffett later tutored Katharine’s son, Don Graham.)

Simple and Understandable

For Buffett, the newspaper business was simple and understandable. Buffett has said that if he were not an investor, he probably would be a journalist.

Consistent Operating History; Favorable Long-Term Prospects

The Washington Post had a consistent operating history and favorable long-term prospects. Newspapers had outstanding economics at the time. (This was in the early 1970s, well before the advent of the internet.) Even mediocre newspapers were generally quite profitable. People and businesses wanting to get a message out to the community would typically use the newspaper to do so. Moreover, newspapers had low capital needs, which meant a high ROIC and high profit margins.

Buy at Attractive Prices

In 1973, the total market value of the Washington Post Company was $80 million. Buffett held that most security analysts, media brokers, and media executives at the time would have estimated WPC’s value at $400 or $500 million. Assuming a $400 million intrinsic value, Buffett was buying at 20 percent of intrinsic value.

Return on Equity and Profit Margins

When Buffett purchased a stake in the WPC, its return on equity (ROE) was 15.7 percent. Within five years, ROE had doubled. WPC maintained a high ROE over the next ten years. At the same time, WPC had paid down most of its debt.

By 1988, pretax margin reached a high of 31.8 percent, compared to 16.9 percent for its newspaper peer group and 8.6% for S&P Industrials.

Management Rationality

Using the gobs of excess cash, between 1975 and 1991, the Washington Post Company repurchased an incredible 43 percent of its shares at relatively low prices.

GEICO Corporation

Leo Goodwin, an insurance accountant, founded the Government Employees Insurance Company (GEICO) in 1936. His idea was to insure only preferred-risk drivers and to sell this insurance directly by mail, bypassing the need for agents or branch offices. Direct selling eliminated overhead expenses equal to 10 to 25 percent of every premium dollar. Goodwin also realized that government employees had fewer accidents than the general public.

(GEICO logo by Dream out loud, via Wikimedia Commons)

Goodwin partnered with a Fort Worth, Texas, banker Cleaves Rhea. Goodwin invested $25,000 for a 25% stake in the business, while Rhea invested $75,000 for a 75% stake in the business. In 1948, the Rhea family decided to sell its interest. Ben Graham decided to buy half Rhea’s stock for $720,000. David Kreeger, a Washington, D.C., lawyer and Lorimer Davidson, a Baltimore bond salesperson, bought the other half.

Lorimer Davidson joined GEICO’s management team and became chairman in 1958. By 1970, GEICO not only had written policies that would lead to underwriting losses; but it also had inadequate reserves. Norman Gidden was tapped to run the company when Davidson retired.

GEICO attempted to grow out of its problems. By 1974, GEICO was facing a potential underwriting loss of $140 million (it turned out to be $126 million). The stock fell from $61 to $5, and was heading lower. GEICO had lost underwriting and cost control discipline.

In 1976, John J. Byrne, a 43-year-old marketing executive from Travelers Corporation, took over as president of GEICO. Meanwhile, the stock drifted down to $2.

Warren Buffett invested $4.1 million at an average price of $3.18.

Simple and Understandable

Back in 1950, Ben Graham–Buffett’s teacher at Columbia University–was a director of GEICO. One Saturday, Buffett went to visit the company in Washington, D.C., to try to learn. A janitor let him in the building, and Buffett ended up getting a 5-hour tutorial from Lorimer Davidson, who was the only executive in the office that day.

Later, when Buffett returned to Omaha and his father’s brokerage firm, he recommended GEICO to the firm’s clients. Buffett himself invested $10,000, two-thirds of his net worth. He sold a year later at a 50 percent profit. Buffett would not invest again in GEICO until 1976.

Buffett owned Kansas City Life and Massachusetts Indemnity & Life Insurance. In 1967, Buffett purchased a controlling interest in National Indemnity. Over the next decade, Buffett learned the insurance business from Jack Ringwalt, the CEO of National Indemnity.

Buffett’s expertise in insurance is what gave him the confidence to invest heavily in GEICO. Between 1976 and 1980, Berkshire invested $47 million in GEICO, 7.2 million shares at an average price of $6.67. The stake was worth $105 million by 1980, representing Buffett’s largest holding.

Consistent Operating History; Favorable Long-Term Prospects

Buffett’s large investment in GEICO seemed to violate the consistent operating history tenet, since GEICO was a turnaround. But Buffett had determined that the essential competitive advantage of the business–providing low-cost agentless insurance–was still intact. Thus, Buffett judged that the problems in 1976, though huge, would ultimately be temporary.

Management Candor and Rationality

Byrne drastically reduced costs. The number of policyholders went from 2.7 million to 1.5 million. GEICO went from being the 18th largest insurer to 31st a year later. But GEICO went from losing $126 million in 1976 to earning an impressive $58.6 million (on $463 million in revenues) in 1977.

Byrne continued to reduce costs. The company stumbled in 1985. But Byrne was very candid about it, and the company quickly recovered. By this point, Byrne had developed a reputation not only for great leadership, but also for candor with shareholders.

From 1983 to 1992, GEICO used excess cash to repurchase 30 million shares, reducing total shares outstanding by 30 percent. GEICO also increased the dividend.

Return on Equity and Profit Margins

In 1980, the ROE at GEICO was 30.8 percent, almost twice as high as the peer group average. Buying back stock and paying dividends helped maintain a high ROE by reducing capital.

GEICO’s combined ratio of corporate expenses and underwriting losses was significantly better than the industry average.

Capital Cities/ABC

![]()

(Wikimedia Commons)

In 1954, Lowell Thomas, the famous journalist; his business manager, Frank Smith; and a group of associates bought Hudson Valley Broadcasting Company, which included an Albany television and AM radio station. At the time, Tom Murphy was a product manager at Lever Brothers.

Frank Smith was a golfing partner of Murphy’s father. Smith hired Murphy to manage the company’s television station. In 1957, the company purchased a Raleigh-Durham television station. The company was renamed Capital Cities Broadcasting, since Albany and Raleigh were capital cities.

In 1960, Murphy hired Dan Burke to manage the Albany station. During the next several decades, Murphy and Burke ran Capital Cities. They made more than 30 acquisitions in broadcasting and publishing.

In the late 1960s, Murphy met Buffett. Murphy invited Buffett to join the board of Cap Cities. Buffett declined, but he and Murphy became good friends.

In early 1985, Murphy obtained an initial agreement for a merger between Cap Cities and ABC. Although Murphy had always done his own deals up until then, this time he brought his friend Warren Buffett. They worked out the largest media merger in history (up to that point). Berkshire Hathaway agreed to purchase three million newly issued shares of Cap Cities at $172.50 per share. Murphy asked Buffett again to join the board, and this time Buffett agreed.

Simple and Understandable

Having served on the Washington Post Company board for more than a decade, Buffett had a very good understanding of television broadcasting, and newspaper and magazine publishing.

Consistent Operating History; Favorable Long-Term Prospects

Both Cap Cities and ABC had more than 30 years of profitable histories. ABC averaged 17 percent ROE from 1975 through 1984. Cap Cities, in the decade before its purchase of ABC, averaged 19 percent ROE. (Both companies also had low debt.)

Hagstrom explains the economics:

Once a broadcasting tower is built, capital reinvestment and working capital needs are minor and inventory investment is nonexistent. Movies and programs can be bought on credit and settled later when advertising dollars roll in. Thus, as a general rule, broadcasting companies produce above-average returns on capital and generate substantial cash in excess of their operating needs.

In 1985, the basic economics were above average.

Determine the Value

Berkshire’s $517 million investment in Cap Cities was the single largest investment Buffett ever made up until then. This was not a cheap price. Buffett joked, ‘I doubt if Ben’s up there applauding me on this one.’

Much of Buffett’s investment depended on Murphy. Operating margins at Cap Cities were 28 percent, but were only 11 percent at ABC. Murphy could improve the margins at ABC.

In essence, Murphy was Buffett’s margin of safety. Murphy and Burke used a decentralized management style, hiring the best people and then leaving them alone to do their job. Managers were expected to operate their businesses as if they owned them. Moreover, Murphy excelled at minimizing costs, while Burke excelled at ongoing operations.

The Institutional Imperative and Rationality

Despite enormous free cash flow, Murphy remained very disciplined about not overpaying for acquisitions. He would sometimes wait for years until the right property at the right price became available.

Because the stock of Cap Cities/ABC was cheap for several years, Murphy repurchased a large number of shares. Murphy also reduced the company’s debt that had resulted from the ABC acquisition.

Buffett viewed Cap Cities/ABC as the best-managed public company in the United States. He assigned all voting rights for the ensuing 11 years to Murphy and Burke as long as at least one of them managed the company.

The Coca-Cola Company

![]()

(Wikimedia Commons)

Hagstrom writes:

By the spring of 1989, Berkshire Hathaway shareholders learned that Buffett had spent $1.02 billion buying Coca-Cola shares. He had bet a third of the Berkshire portfolio, and now owned 7 percent of the company. It was the single-largest Berkshire investment to date, and already Wall Street was scratching its head. Buffett had paid five times book value and over 15 times earnings, then a premium to the stock market, for a hundred-year-old company that sold soda pop. What did the Wizard of Omaha see that everyone else missed?

As a kid, Buffett would buy six Cokes for 25 cents, then resell them at 5 cents each. And in 1986, Buffett announced that Cherry Coke would be the official soft drink at Berkshire Hathaway’s annual meetings. But it wasn’t until 1988 that Buffett began buying shares.

Simple and Understandable

The company sells a concentrate to bottlers, who combine it with other ingredients and then sell the finished product to retail outlets. The company also sells soft drink syrups to restaurants and fast-food retailers.

Consistent Operating History; Favorable Long-Term Prospects

Buffett explained in an interview with Melissa Turner of the Atlanta Constitution his reasoning: If he could make one investment and then go away for ten years without access to any information about the investment, what would he buy? As far as remaining a worldwide leader and experiencing big ongoing unit growth, there was nothing (in 1989) like Coke.

Furthermore, the chairman and CEO of Coke, Roberto Goizueta, and the president Donald Keough, were doing an outstanding job erasing mistakes that had been made in the 1970s. Robert Woodruff, the company’s 91-year-old patriarch, hired Roberto Goizueta in 1980. Goizueta cut costs and demanded that any business owned by Coca-Cola maximize return on assets.

High Profit Margins and ROE

Under Goizueta and Keough, pretax margins rose from 12.9 percent to a record 19 percent by 1988. Goizueta sold any business that did not generate good ROE. By 1988, the company’s ROE reached 31 percent, up from 20 percent during the 1970s.

Management Candor and Rationality

Under Goizueta’s leadership, Coke’s mission became crystal clear: maximize shareholder value over time. This would be achieved by optimizing profit margins and ROE.

Meanwhile, Goizueta announced that the company would repurchase shares, which were trading at a discount to the company’s now-higher intrinsic value.

The Institutional Imperative

Hagstrom describes Goizueta’s leadership:

When Goizueta took over Coca-Cola, one of his first moves was to jettison the unrelated businesses that Paul Austin had developed, and return the company to its core business: selling syrup. It was a clear demonstration of Coca-Cola’s ability to resist the institutional imperative.

Reducing the company to a single-product business was undeniably a bold move…

… Because the economic returns of selling syrup far outweighed the economic returns of the other businesses, the company was now reinvesting its profits in its highest-return business.

Determine the Value

Buffett paid 5 times book value, 15 times earnings, and 12 times cash flow. This was at a time when long-term bonds were yielding 9 percent. Hagstrom:

…The company was earning 31 percent on equity while employing relatively little in capital investment. Buffett has explained that price tells you nothing about value. The value of Coca-Cola, he said, like that of any other company, is determined by the total owner earnings expected to occur over the life of the business, discounted by the appropriate interest rate.

Owner earnings is the term Buffett uses for free cash flow (FCF). We can use a two-stage discount model to calculate the present value in 1988. Assuming 15 percent growth in owner earnings for the next 10 years, and then 5 percent growth thereafter, and assuming a 9 percent discount rate, intrinsic value for Coca-Cola would be $48.377 billion. That’s compared to the 1988 market value of $14.8 billion.

At year-end 1999, the market value of Coke was $143 billion, and Berkshire’s original $1.02 billion investment was worth $11.6 billion.

General Dynamics

In 1990, General Dynamics was the country’s second-largest defense contractor behind McDonnell Douglas Corporation. General Dynamics produced missile systems in addition to air defense systems, space-launched vehicles, and fighter planes for the U.S. armed forces.

![]()

(Wikimedia Commons)

In January 1991, General Dynamics appointed William Anders as CEO. Within six months, the company had raised $1.25 billion by selling noncore businesses. With the cash, the company first paid down its debt. Then as excess cash flow continued, General Dynamics purchased 13.2 million shares at prices between $65.37 and $72.25, reducing its shares outstanding by 30 percent.

Although Buffett initially had purchased General Dynamics as an arbitrage–in anticipation of stocks buybacks–Buffett later noticed that Anders was very focused on maximizing shareholder value. So Buffett held the stake:

From July 1992 through the end of 1993, for its investment of $72 per share, Berkshire received $2.60 in common dividends, $50 in special dividends, and a share price that rose to $103. It amounted to a 116 percent return over 18 months.

Wells Fargo & Company

In October 1990, Buffett announced that Berkshire had purchased five million shares in Wells Fargo, investing $289 million at an average price of $57.88 per share. This turned into a battle between bulls like Buffett and bears like the Feshbach brothers.

(Wikimedia Commons)

Buffett knew a lot about the business of banking. In 1969, Berkshire Hathaway purchased 98 percent of the holdings of Illinois National Bank and Trust Company. Gene Abegg, the chairman of Illinois National Bank, taught Buffett about the banking business. Buffett learned that banks were profitable if they issued loans intelligently and curtailed costs.

Favorable Long-Term Prospects

When assets are 20 times equity, which is normal in banking, even a small mistake can cause the bank to go bankrupt. But if management does a good job, a bank can earn 20 percent on equity, which is above the average of most businesses. Also, Buffett believed he had the best management team in Carl Reichardt and Paul Hazen. Buffett: “In many ways, the combination of Carl and Paul reminds me of another–Tom Murphy and Dan Burke at Capital Cities/ABC.”

Munger explained: ‘It’s all a bet on management. We think they will fix the problems faster and better than other people.”

Rationality

Reichardt was legendary for relentlessly lowering costs. He never let up, always searching for ways to improve profitability.

American Express Company

![]()

(Wikimedia Commons)

Buffett: “I find that a long-term familiarity with a company and its products is often helpful in evaluating it.” Hagstrom explains:

With the exception of selling bottles of Coca-Cola for a nickel, delivering copies of the Washington Post, and recommending that his father’s clients buy shares of GEICO, Buffett has had a longer history with American Express than any other company Berkshire owns. You may recall that in the mid-1960s, the Buffett Limited Partnership invested 40 percent of its assets in American Express shortly after the company’s losses in the salad oil scandal. Thirty years later, Berkshire accumulated 10 percent of American Express shares for $1.4 billion.

Consistent Operating History

American Express was essentially the same business when Berkshire invested as it had been when the Buffett partnership invested. Travel Related Services (TRS) made up 72 percent of American Express’s sales. American Express Financial Advisors represented 22 percent of sales. American Express Bank was about 5%.

Under James Robinson, the company used excess cash to acquire related business. Although IDS (renamed American Express Financial Advisors) had proved to be a profitable purchase, Robinson’s $4 billion investment in Shearson-Lehman was a financial drain and prompted Robinson to contact Buffett. Buffett was willing to buy $300 million in preferred shares. But Buffett was not ready to invest in the common shares until he saw more management rationality.

Rationality

In 1992, Harvey Golub took over as CEO. Golub clearly recognized the brand value of the American Express Card. Over the next two years, Golub sold off American Express’s underperforming assets, and restored profitability and high ROE. By 1994, American Express management was focused on making the American Express Card the “world’s most respected service brand.”

Golub also set financial targets: to increase EPS by 12 to 15 percent annually and to achieve an 18 to 20 percent ROE. Management was also planning to repurchase 20 million shares of its common stock.

In the summer of 1994, Buffett converted Berkshire’s preferred issue into American Express common stock. And he began to acquire even more shares of common stock. Berkshire owned 27 million shares at an average price of $25 by the end of the year. When American Express finished repurchasing 20 million shares, it announced that it would repurchase an additional 40 million shares, or 8 percent of the stock outstanding. By March 1995, Buffett had added another 20 million shares, which increased Berkshire’s ownership to a bit less than 10 percent of American Express.

Determine the Value

Assuming 12 percent growth in owner earnings for 10 years, then 5 percent growth thereafter, and assuming a discount rate of 10 percent–which is conservative–the intrinsic value of American Express at the end of 1994 was about $50 billion, or $100 per share. Thus Buffett’s purchase of 27 million shares at $25 had a significant margin of safety, and therefore significant potential upside.

International Business Machines

Buffett had always avoided investing in technology companies because constant disruption and innovation make for very short company life spans. But by the end of 2011, Berkshire Hathaway had purchased 63.9 million shares of IBM, or 5.4 percent of the company. At $10.8 billion, it was the largest purchase of individual stock Buffett has ever made.

![]()

(Photo by Paul Rand, via Wikimedia Commons)

Favorable Long-Term Prospects

After 50 years of reading the financial statements of IBM, Buffett suddenly realized the competitive advantages IBM has in finding and keeping clients. IBM dominates information technology (IT) services, which includes consulting, systems integration, IT outsourcing, and business process outsourcing. IBM is number-one globally in the consulting and systems integration space, and number-one globally in IT outsourcing.

Revenues from IT services are relatively stable. Consulting, systems integration, and IT outsourcing are even thought to possess ‘moat-like’ qualities, writes Hagstrom. In consulting and systems integration, intangible assets like reputation, track record, and client relationships are sources of a moat. In IT outsourcing, switching costs and scale advantages create a moat.

J. Heinz Company

On February 14, 2013, Berkshire Hathaway and 3G Capital purchased H. J. Heinz Company for $23 billion. The purchase price was $72.50 a share, a 20 percent premium to the stock price the day before.

![]()

(Wikimedia Commons)

Favorable Long-Term Prospects; Rationality

Heinz is number one in ketchup globally and second in sauces. The company is poised to do well in rapidly growing emerging markets.

Buffett has partnered with 3G Capital in the purchase of Heinz. 3G has a track record of relentlessly lowering costs.

Holding Period: Forever

Buffett is “quite content to hold any security indefinitely, so long as the prospective return on equity capital of the underlying business is satisfactory, management is competent and honest, and the market does not overvalue the business.”

PORTFOLIO MANAGEMENT: THE MATHEMATICS OF INVESTING

If you do not have the time or inclination to study companies in depth, then a low-cost index fund is best. But if you can understand some businesses, then a concentrated portfolio makes sense.

There is a mathematical formula, the Kelly criterion, that you can use to get an idea of how large a position to take on your best ideas. The formula was invented by the physicist John L. Kelly.

(John L. Kelly, Wikimedia Commons)

Buffett talked about index funds vs. focused portfolios in the 1993 Berkshire Hathaway Letter to Shareholders:

By periodically investing in an index fund, for example, the know-nothing investor can actually out-perform most investment professionals. Paradoxically, when ‘dumb’ money acknowledges its limitations, it ceases to be dumb.

On the other hand, if you are a know-something investor, able to understand business economics and to find five to ten sensibly-priced companies that possess important long-term competitive advantages, conventional diversification makes no sense for you. It is apt simply to hurt your results and increase your risk. I cannot understand why an investor of that sort elects to put money into a business that is his 20th favorite rather than simply adding that money to his top choices–the businesses he understands best and that present the least risk, along with the greatest profit potential.

Here is Buffett in a 1998 lecture at the University of Florida:

If you can identify six wonderful businesses, that is all the diversification you need. And you will make a lot of money. And I can guarantee that going into the seventh one instead of putting more money into your first one is [going to] be a terrible mistake. Very few people have gotten rich on their seventh best idea. So I would say for anyone working with normal capital who really knows the businesses they have gone into, six is plenty, and I [would] probably have half of [it in] what I like best.

Link: http://intelligentinvestorclub.com/downloads/Warren-Buffett-Florida-Speech.pdf

Even in a highly focused portfolio of 5 to 10 stocks, often your best idea should be by far the largest position in your portfolio.

Recall that Buffett invested two-thirds of his net worth in GEICO before he launched the Buffett partnership. He had over a 50 percent profit after a year. Later, Buffett invested 40 percent of the Buffett partnership in American Express. The shares nearly tripled over the next two years. A couple of decades later, Buffett invested $1.02 billion–about a third of Berkshire Hathaway’s portfolio–in Coca-Cola. This turned out to be a 10-bagger for Berkshire, netting $10 billion in profit over the ensuing decade.

It can be tempting for an investor to listen to forecasters predict the stock market, the economy, or elections. But owning a few good businesses over time is a far more reliable and safer way to compound your capital–at higher rates–than speculating on the stock market or the economy.

Here are a few good quotes from Buffett on forecasting:

- I don’t invest a dime based on macro forecasts.

- Market forecasters will fill your ear but never fill your wallet.

- We will continue to ignore political and economic forecasts, which are an expensive distraction for many investors and businessmen.

- Charlie and I never have an opinion on the market because it wouldn’t be any good and it might interfere with the opinions we have that are good.

Hagstrom puts it as follows:

In shorter periods, we realize that changes in interest rates, inflation, or near-term expectations for a company’s earnings can affect share prices. But as the time horizon lengthens, the trendline economics of the underlying business will increasingly dominate its share price.

… Focus investors tolerate the [short-term] bumpiness because they know that, in the long run, the underlying economics of the companies will more than compensate for any short-term price fluctuations.

Investing is Probabilistic

(Photo by Michele Lombardo)

Nearly all investments are probabilistic decisions, or decisions under uncertainty. Hagstrom quotes Buffett:

Take the probability of loss times the amount of possible loss from the probability of gain times the amount of possible gain. That is what we’re trying to do. It’s imperfect but that’s what it is all about.

Hagstrom also quotes Charlie Munger:

The model I like–to sort of simplify the notion of what goes on in a market for common stocks–is the pari-mutuel system at the racetrack. If you stop and think about it, a pari-mutuel system is a market. Everybody goes there and bets and the odds are changed based on what’s bet. That’s what happens in the stock market.

Any damn fool can see that a horse carrying a light weight with a wonderful win rate and good position et cetera is way more likely to win than a horse with a terrible record and extra weight and so on and so on. But if you look at the odds, the bad horse pays 100 to 1, whereas the good horse pays 3 to 2. Then it’s not clear which is statistically the best bet. The prices have changed in such a way that it’s very hard to beat the system.

When you find a high-probability bet with substantial upside–which will only happen rarely–then you should take a big position. How big? You have to know yourself in terms of how much portfolio volatility you can tolerate. As long as you can hold for the longer term–for at least 5 or 10 years–without reacting to shorter term volatility, then it makes sense to take large positions on the best ideas you find.

If you apply the Kelly criterion to a focused portfolio of value stocks, then you typically need to normalize positions sizes. Mohnish Pabrai has explained this: https://boolefund.com/the-dhandho-investor/

John Maynard Keynes was very successful as a focused value investor: https://boolefund.com/greatest-economist-defied-convention-got-rich/

Hagstrom has a quote from Keynes:

It is a mistake to think one limits one’s risk by spreading too much between enterprises which one knows little and has no reason for special confidence… One’s knowledge and experience are definitely limited and there are seldom more than two or three enterprises at any given time in which I personally feel myself entitled to put full confidence.

Keynes was against market timing, and in favor of a very concentrated portfolio.

Hagstrom also mentions Ruane, Cuniff & Company, started by Bill Ruane and Rick Cuniff. They would have 90 percent of the fund in 6 to 10 positions.

Lou Simpson used a very concentrated approach when he managed GEICO’s equity portfolio. Between 1980 and 2004, GEICO’s portfolio returned 20.3 percent per year compared to 13.5 percent for the market.

Active share is the percentage of a portfolio that differs from the benchmark index holdings. The only way to do better than the index is to invest differently. Yet most professional investors have portfolios not much different than the index. They are more worried about not underperforming the index than they are focused on doing better than the index. Hagstrom reports that just 25 percent of mutual funds today are considered truly active.

Moreover, many professional investors are focused on short-term results. The problem is that the performance of a portfolio of stocks is largely random for time horizons less than 5 years. That is why Buffett focuses on 5-year periods to measure Berkshire Hathaway’s performance. After 5 years–and even more after 10 years–a stock will track the performance of the underlying business.

Many professional investors fixate on quarterly or annual results because many of their clients (or potential clients) decide to invest in the fund based on these short-term results.

Many of the best long-term investors have had periods of significant underperformance over shorter periods of time. When Keynes managed the Chest Fund, it underperformed the market one-third of the time. This includes underperforming the market by 18 percentage points in the first three years Keynes managed the fund. But Keynes’ record over a couple of decades was outstanding.

The Sequoia Fund, managed by Bill Ruane, underperformed the market 37 percent of the time. In fact, Sequoia underperformed for the first 4 years of its existence. By the end of 1974, the fund was 36 percentage points behind the market. Yet three years later–seven years since inception–Sequoia was up 220 percent, versus 60 percent for the S&P 500 Index.

Over 14 years, Charlie Munger underperformed 36 percent of the time. But Munger’s overall record was far better than the market. (Lou Simpson underperformed the market 24 percent of the time, but also had a remarkable long-term record of beating the market.)

If you’re a long-term investor in businesses–whether public or private–what matters over time is the economic performance of those businesses, not the prices at which the businesses can be bought or sold. Hagstrom:

If you owned a business and there were no daily quotes to measure its performance, how would you determine your progress? Likely you would measure the growth in earnings, the increase in return on capital, or the improvement in operating margins. You simply would let the economics of the business dictate whether you were increasing or decreasing the value of your investment.

Hagstrom quotes Buffett:

While market values track business values quite well over long periods, in any given year the relationship can gyrate capriciously.

Buffett again:

The speed at which a business’s success is recognized… is not that important as long as the company’s intrinsic value is increasing at a satisfactory rate. In fact, delayed recognition can be an advantage: It may give you a chance to buy more of a good thing at a bargain price.

When you consider a new investment idea, you should always compare it to the best ideas already in your portfolio. Since good ideas are rare, this should set a high threshold and screen out 99 percent of what you consider. Hagstrom observes:

You already have at your disposal, with what you now own, an economic benchmark–a measuring stick. You can define your own personal benchmark in several different ways: look-through earnings, return on equity, or margin of safety, for example. When you buy or sell stock of a company in your portfolio, you have either raised or lowered your economic benchmark. The job of a portfolio manager who is a long-term owner of securities, and who believes future stock prices eventually will match with underlying economics, is to find ways to raise your benchmark.

If you step back and think for a moment, the Standard & Poor’s 500 index is a measuring stick. It is made up of 500 companies and each has its own economic return. To outperform the S&P 500 index over time–to raise that benchmark–we have to assemble and manage a portfolio of companies with economics that are superior to the average weighted economics of the index.

Buffett:

If my universe of business possibilities was limited, say, to private companies in Omaha, I would, first, try to assess the long-term economic characteristics of each business. Second, assess the quality of the people in charge of running it; and third, try to buy into a few of the best operations at a sensible price. I certainly would not wish to own an equal part of every business in town. Why, then, should Berkshire take a different tack when dealing with the larger universe of public companies? And since finding great businesses and outstanding managers is so difficult, why should we discard proven products? Our motto is: If at first you succeed, quit trying.

Buffett again:

Inactivity strikes us as an intelligent behavior. Neither we nor most business managers would dream of feverishly trading highly profitable subsidiaries because a small move in the Federal Reserve’s discount rate was predicted or because some Wall Street pundit has reversed his views on the market. Why, then, should we behave differently with our minority positions in wonderful businesses?

Buying and holding wonderful businesses has two important benefits in addition to growing capital at an above-average rate. Transaction costs are kept to an absolute minimum, and after-tax returns are maximized.

Buffett gives an example of $1 doubling every year for 20 years. First assume that you sell and pay tax at the end of each year. So after the first year, you would have a total of $1.66. By the end of 20 years, you would have a net gain of $25,200, after paying taxes of $13,000. By contrast, if you held the $1 dollar as it repeatedly doubled, and didn’t sell until the end of the 20-year period, you would have $692,000 after paying taxes of about $356,000.

To achieve high after-tax returns, turnover should be between 0 and 20 percent. 20 percent turnover implies a 5-year holding period. As long as you are very patient and can stay focused on the long term without reacting emotionally to shorter term volatility, you should be able to construct and stick with a focused portfolio of businesses that you understand. Always being rational and not reacting out of emotion is more important than IQ. Buffett:

You don’t need to be a rocket scientist. Investing is not a game where the 160 IQ guy beats the guy with the 130 IQ. The size of an investor’s brain is less important than his ability to detach the brain from the emotions.

THE PSYCHOLOGY OF INVESTING

Although it’s not widely recognized, Ben Graham was keenly aware of the importance of psychology for investors. Graham held that your worst enemy as an investor is usually yourself.

Warren Buffett, Graham’s most famous student, says there are three important principles in Graham’s approach to investing:

- Stock is a fractional ownership in a business. What matters for the investor is how the business performs over time.

- Margin of safety: Given a reasonable estimate of intrinsic value–based on net asset value or earnings power–you should only buy when the price is well below that estimate. The lower the price is compared to intrinsic value, the safer the investment and simultaneously the higher the potential reward.

- Short-term price fluctuations have no meaning for the true investor because on the whole they do not reflect changes in business value. Fluctuations do occasionally create opportunities, however, for the investor to buy if the price becomes cheap enough.

When the stock price drops, a rational investor’s reaction should be the same as a businessperson who gets a lowball offer on his or her privately owned business: Ignore it. Graham:

The true investor scarcely ever is forced to sell his shares and at all other times is free to disregard the current price quotation.

Behavioral Finance

(Daniel Kahneman, via Wikimedia Commons)

Behavioral finance is based on discoveries (in the past few decades) in psychology by Daniel Kahneman, Amos Tversky, and many others. Kahneman was awarded the Nobel Prize in economics in 2002 for discoveries that he and Tversky made from decades of experiments of people making decisions under uncertainty.

Before Kahneman and Tversky, economists always assumed–based on utility theory as described by John von Neumann and Oskar Morgenstern–that people make rational decisions under uncertainty. (Investment decisions are decisions under uncertainty.)

We now know that nearly all investors make systematic errors. Behavioral finance allows us to understand these errors.

Overconfidence, Confirmation Bias, Availability Bias

People by nature are overconfident. Typically if you ask people in a random group how good a driver they are, at least 80-90 percent will say ‘above average.’ But of course no more than 50% can be above average.

In many areas of life, overconfidence is not bad and often even is helpful. When we were hunter-gatherers, it was a net benefit for the tribe if hunters were individually overconfident. Similarly today, although many entrepreneurs fail, it is a net benefit for the economy that nearly all entrepreneurs believe they will succeed.

When you are investing, however, overconfidence will penalize your results over time. Hagstrom points out:

Investors, as a rule, are highly confident they are smarter than everyone else. They have a tendency to overestimate their skills and their knowledge. They typically rely on information that confirms what they believe, and disregard contrary information. In addition, the mind works to assess whatever information is readily available rather than to seek out information that is little known….

Overconfidence explains why so many money managers make wrong calls. They take too much confidence from the information they gather, and think they are more right than they actually are.

Confirmation bias means only seeing information that confirms what you already believe, rather than seeking and being aware of potentially disconfirming information. Availability bias means only noticing information that is readily available.

Overreaction Bias

Overreaction Bias means investors overreact to bad news and react slowly to good news. If there is bad news and the stock price drops, an investor is likely to overreact and to sell, even though the long-term, underlying economics of the business are often unchanged.

Richard Thaler researched overreaction. He constructed a portfolio of ‘Loser’ stocks–stocks that had been the worst performers over the preceding 5 years. He compared the ‘Loser’ portfolio to a portfolio of ‘Winner’ stocks–stocks that had performed best over the preceding 5 years. Thaler found that over the subsequent 5 years, the ‘Loser’ portfolio far outperformed both the market and the ‘Winner’ portfolio.

Loss Aversion

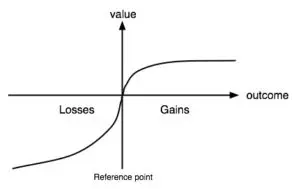

People are risk averse when considering potential gains, but risk seeking when facing the possibility of a certain loss. This is the essence ofprospect theory–invented by Kahneman and Tversky–which is captured in the following graph:

(Value function in Prospect Theory, drawing by Marc Rieger, via Wikimedia Commons)

Loss aversion means that, in general, people feel a loss 2 to 2.5 times more than an equivalent gain. (That’s why the value function in the graph is steeper for losses.) Therefore, when people are presented with a 50/50 bet, on average they will only bet if the potential gain is at least twice as large as the potential loss.

Loss aversion causes people to hold on to their losing investments for too long. By not selling an investment that hasn’t worked, the investor can postpone the feeling of a loss. Yet the sooner the investor can recognize a mistake and close the position, the sooner the investor can reinvest that capital in a potentially more profitable way.

Mistakes in investing are inevitable. Even for the best value investors, on average they tend to be right about two-thirds of the time and wrong one-third of the time. The best investors can recognize quickly when either they have made a mistake or when unforeseeable events have invalidated the investment thesis.

Long-Term Investment Time Horizon

Warren Buffett focuses on the performance of the business over a 5-year or 10-year period. He invests in a stock when it is a bargain relative to the probable long-term earnings power of the business.

Many investors are way too focused on the short term. The problem is that if you check a stock price each day, there is 50 percent chance it will be lower. And due to loss aversion, you will feel the pain of a lower price at least twice as much as the pleasure of an equivalent gain. Therefore, after carefully constructing your portfolio, it’s essential to stay focused on the performance of the businesses over rolling 5-year periods. It’s also essential to check stock prices as infrequently as you can.

Very often the individual investors who have gotten the best results over the course of 20-30 years are those investors who effectively forgot about their investments. These investors often didn’t check stock prices for years at a time. As Ben Graham said, for many investors it would be better if they couldn’t get any stock quote at all.

Warren Buffett has often said you should only invest in a business where you wouldn’t worry at all if the stock market closed for 5 or 10 years. All that matters for the long-term value investor is how the underlying business performs over time. If it’s a good business that increases earnings and maintains a high return on capital over time, then your fractional ownership of the business will track the increase in intrinsic value.

THE VALUE OF PATIENCE

Too many investors have the mistaken belief that the stock market can be predicted. But it can’t. Ben Graham:

[If] I have noticed anything over these 60 years on Wall Street, it is that people do not succeed in forecasting what’s going to happen to the stock market.

Hagstrom did some research about long-term investing, and here is what he found:

We calculated the one-year return, trailing three-year return, and trailing five-year return (price only) between 1970 and 2012. During this 43-year period, the average number of stocks in the S&P 500 index that doubled in any one year averaged 1.8 percent, or about nine stocks out of 500. Over three-year rolling periods, 15.3 percent of stocks doubled, about 77 stocks out of 500. In rolling five-year blocks, 29.9 percent doubled, about 150 out of 500.

So, back to the original question: Over the long term, do large returns from buying and holding stocks actually exist? The answer is indisputably yes. And unless you think a double over five years is trivial, this equates to a 14.9 percent average annual compounded return.

Then Hagstrom notes that the greatest number of opportunities to get high excess returns is after three years. So, as an investor, you should patiently find cheap and good stocks that you can hold for at least 3 to 5 years. There continue to be many opportunities over this time frame because many investors only look at the very short term. The average holding period is only a few months, which is hardly different from a coin flip.

Rationality

Keith Stanovich holds that rationality is not the same thing as intelligence. He says IQ tests or SAT/ACT exams do a poor job of measuring rational thought:

It is a mild predictor at best, and some rational thinking skills are totally dissociated from intelligence.

There appear to be two main reasons why even many high IQ people are not able to think rationally: a processing problem and a content problem.

To understand the processing problem, we must first note that we have essentially two different brains: System 1 and System 2.

System 1 operates automatically and quickly. It makes instinctual decisions based on heuristics.

System 2 allocates attention (which has a limited budget) to the effortful mental activities that demand it, including complex computations involving logic, math, or statistics.

Usually System 1 and System 2 work well together, but not always. Daniel Kahneman explains in his great book, Thinking, Fast and Slow:

The division of labor between System 1 and System 2 is highly efficient: it minimizes effort and optimizes performance. The arrangement works well most of the time because System 1 is generally very good at what it does: its models of familiar situations are accurate, its short-term predictions are usually accurate as well, and its initial reactions to challenges are swift and generally appropriate. System 1 has biases, however, systematic errors that it is prone to make in specified circumstances… it sometimes answers easier questions than the one it was asked, and it has little understanding of logic and statistics. One further limitation of System 1 is that it cannot be turned off.

If the situation requires a complex computation in order to arrive at a good decision, then System 1 makes predictable errors. In order to avoid these mistakes, a person must train his or her System 2 to activate and to think carefully.

So the processing problem requires training System 2. But there is a second problem the investor also must solve: the content problem. The ability to think rationally using System 2 can only lead to good decisions if System 2 has access to enough mindware. Mindware–as defined by Harvard cognitive scientist David Perkins–is all the rules, strategies, procedures, and knowledge people have at their disposal to help solve a problem.

In investing, the most important thing is reading a great deal, especially the financial statements of various companies. Over time, an investor can slowly develop useful mindware.

THE WORLD’S GREATEST INVESTOR

To determine how good Warren Buffett is, there are two basic variables: relative outperformance and duration. Hagstrom argues that both are needed. Over shorter periods of time, luck plays a large role. But as you extend out in time–several decades and then some–luck plays less and less of a role.

Buffett has crushed the market over a period of almost 60 years. Buffett is unmatched over this time frame.

Buffett also remains very bullish on the United States. He says the luckiest new babies in history are those being born today:

…Warren Buffett is unabashedly bullish on the United States of America. He has never been shy to express his belief that the United States offers tremendous opportunity to anyone who is willing to work hard. He is upbeat, cheerful, and optimistic about life in general. Conventional wisdom holds that it is the young who are the eternal optimists and as you get older pessimism begins to tilt the scale. But Buffett appears to be the exception. And I think part of the reason is that for almost six decades he has managed money through a long list of dramatic and traumatic events, only to see the market, the economy, and the country recover and thrive.

It is a worthwhile exercise to Google the noteworthy events of the 1950s, 1960s, 1970s, 1980s, 1990s, and the first decade of the twenty-first century. Although too numerous to list here, the front-page headlines would include nuclear war brinksmanship; presidential assassination and resignation; civil unrest and riots; regional wars; oil crisis, hyperinflation, and double-digit interest rates; and terrorist attacks–not to mention the occasional recession and periodic stock market crash.

Hagstrom proceeds to argue that Buffett has three advantages: behavioral, analytical, and organizational.

Behavioral Advantage

Those who know Buffett agree that it is rationality that sets him apart. Buffett is extremely rational. As Roger Lowenstein writes in Buffett: The Making of an American Capitalist, “Buffett’s genius [is] largely a genius of character–of patience, discipline, and rationality.” The maximization of shareholder value depends largely on the rational allocation of capital. This is a key trait Buffett looks for in good managers, and it’s a trait he himself has to a remarkable degree.

Analytical Advantage

For Buffett, both the investor and the businessperson should look at a company in terms of how much cash it can produce over time. By recognizing, furthermore, that short-term stock prices are largely random, you can learn to value a business–based on discounted FCF or net asset value–and wait patiently until its stock price is well below intrinsic value.