There are many ways to get rich. One of the best ways is through long-term investing.

A wise long-term investment for most investors is an S&P 500 index fund. It’s just simple arithmetic, as Warren Buffett and Jack Bogle frequently observe: https://boolefund.com/warren-buffett-jack-bogle/

But you can do significantly better–roughly 18% per year (instead of 10% per year)–by systematically investing in cheap, solid microcap stocks.

Most professional investors never consider microcaps because their assets under management are too large. Microcaps aren’t as profitable for them. That’s why there continues to be a compelling opportunity for savvy investors. Because microcaps are largely ignored, many get quite cheap on occasion.

The smallest two deciles – 9+10 – comprise microcap stocks, which typically are stocks with market caps below $500 million. What stands out is the equal weighted returns of the 9th and 10th size deciles from 1927 to 2020:

Microcap equal weighted returns = 15.8% per year

Large-cap equal weighted returns = ~10% per year

In practice, the annual returns from microcap stocks will be 1-2% lower because of the difficulty (due to illiquidity) of entering and exiting positions. So we should say that an equal weighted microcap approach has returned 14% per year from 1927 to 2020, versus 10% per year for an equal weighted large-cap approach.

Still, if you can do 4% better per year than the S&P 500 Index (on average) – even with only a part of your total portfolio – that really adds up after a couple of decades.

Most professional investors ignore micro caps as too small for their portfolios. This causes many micro caps to get very cheap. And that’s why an equal weighted strategy – applied to micro caps – tends to work well.

VALUE SCREEN: +2-3%

By systematically implementing a value screen–e.g., low EV/EBITDA or low P/E–to a microcap strategy, you can add 2-3% per year.

GROWING EARNINGS AND IMPROVING FUNDAMENTALS: +2-3%

You can further boost performance by screening for growing earnings and improving fundamentals. One excellent way to do this is using the Piotroski F_Score, which works best for cheap micro caps. See: https://boolefund.com/joseph-piotroski-value-investing/

This screen should increase performance by at least 2-3% a year.

POSITIVE MOMENTUM AND OTHER FACTORS: +2-3%

Then our model screens for high shareholder yield, high insider ownership, insider buying, high ROE, low/no debt, and positive momentum. This screen should further boost performance by at least 2-3% a year.

BOTTOM LINE

If you invest in microcap stocks, you can get about 14% a year. If you also use a simple screen for value, that adds at least 2-3% a year. If, in addition, you screen for growing earnings and improving fundamentals, that adds at least another 2-3% a year. Finally, screening for positive momentum and others factors boosts performance at least another 2-3% a year. So that takes you to 20-23% a year. After fees, that comes to 15-18% a year, which compares quite well to the 10% a year you could get from an S&P 500 index fund.

What’s the difference between 15% a year and 10% a year? If you invest $50,000 at 10% a year for 30 years, you end up with $872,000, which is good. If you invest $50,000 at 15% a year for 30 years, you end up with $3.31 million, which is much better.

Please contact me if you would like to learn more.

My email: jb@boolefund.com.

My cell: 206.518.2519

BOOLE MICROCAP FUND

An equal weighted group of micro caps generally far outperforms an equal weighted (or cap-weighted) group of larger stocks over time.

This outperformance increases significantly by focusing on cheap micro caps. Performance can be further boosted by isolating cheap microcap companies with improving fundamentals and positive momentum. We rank microcap stocks based on these and similar criteria.

There are roughly 10-15 positions in the portfolio. The size of each position is determined by its rank. Typically the largest position is 15-20% (at cost), while the average position is 8-10% (at cost). Positions are held for 3 to 5 years unless a stock approaches intrinsic value sooner or an error has been discovered.

The mission of the Boole Fund is to outperform the S&P 500 Index by at least 5% per year (net of fees) over 5-year periods. We also aim to outpace the Russell Microcap Index by at least 2% per year (net). The Boole Fund has low fees.

If you are interested in finding out more, please e-mail me or leave a comment.

My e-mail: jb@boolefund.com

Disclosures: Past performance is not a guarantee or a reliable indicator of future results. All investments contain risk and may lose value. This material is distributed for informational purposes only. Forecasts, estimates, and certain information contained herein should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed.No part of this article may be reproduced in any form, or referred to in any other publication, without express written permission of Boole Capital, LLC.

Warren Buffett, arguably the greatest investor of all time, was the only student to whom professor Ben Graham gave an A+ for the course he taught on security analysis at Columbia University. Buffett later worked for Graham for a couple of years. Graham was a teacher, a mentor, and a friend to Buffett. Buffett said about Ben Graham’s The Intelligent Investor:

Chapters 8 and 20 have been the bedrock of my investing activities for more than 60 years. I suggest that all investors read those chapters and reread them every time the market has been especially strong or weak.

(Ben Graham, by Equim43 via Wikimedia Commons)

CHAPTER 8: THE INVESTOR AND MARKET FLUCTUATIONS

Graham notes that stock prices fluctuate widely, and the intelligent investor should be interested in profiting from these swings. Graham says there are two ways to do this: timing and pricing. Timing is an attempt to predict stock prices. Graham:

By pricing we mean the endeavor to buy stocks when they are quoted below their fair value and to sell them when they rise above such value.

Note that fair value, also called intrinsic value, is how much a knowledgeable buyer would pay for a business, based either upon how much the business can earn or based upon the balance sheet of the business.

Graham continues by noting that trying to time the market is speculation, and will not result in profits over the long term. Many investors feel compelled to listen to stock market forecasts. But, says Graham:

There is no basis either in logic or in experience for assuming that any typical or average investor can anticipate market movements more successfully than the general public, of which he is himself a part.

This is understating the case. There is no evidence that any individual forecaster has been able to consistently predict the short-term movements of the stock market.

Illustration by Maxim Popov

Graham points out that one factor that leads the speculator to rely on shorter-term stock market predictions is that the speculator is in a hurry to make money. An investor, by contrast, does not mind waiting one year or several years for a sound investment to pay off.

Furthermore, timing formulas based on the past tend not to work as well in the future, as Graham explains:

Those formulas that gain adherents and importance do so because they have worked well over a period, or sometimes merely because they have been plausibly adapted to the statistical record of the past. But as their acceptance increases, their reliability tends to diminish. This happens for two reasons: First, the passage of time brings new conditions which the old formula no longer fits. Second, in stock-market affairs the popularity of a trading theory has itself an influence on the market’s behavior which detracts in the long run from its profit-making possibilities.

Graham writes of several theories that tried to identify buying conditions and selling conditions in the market. Even Graham himself developed a “central value method.” However, says Graham:

The moral seems to be that any approach to moneymaking in the stock market which can be easily described and followed by a lot of people is by its terms too simple and too easy to last.

An an investor, one should expect wide fluctuations in stock prices. But what do you do after stock prices have advanced a great deal? Graham:

But has the price risentoo high, and should you think of selling? Or should you kick yourself for not having bought more shares when the level was lower? Or–worst thought of all–should you now give way to the bull-market atmosphere, become infected with the enthusiasm, the overconfidence and the greed of the great public (of which, after all, you are a part), and make larger and dangerous commitments? Presented thus in print, the answer to the last question is a self-evident no, but even the intelligent investor is likely to need considerable will power to keep from following the crowd.

Graham continues:

It is for these reasons of human nature, even more than by calculation of financial gain or loss, that we favor some kind of mechanical method for varying the proportion of bonds to stocks in the investor’s portfolio. The chief advantage, perhaps, is that such a formula will give himsomething to do. As the market advances he will from time to time make sales out of his stockholdings, putting the proceeds into bonds; as it declines he will reverse the procedure. These activities will provide him some outlet for his otherwise too-pent-up energies. If he is the right kind of investor he will take added satisfaction from the thought that his operations are exactly opposite from those of the crowd.

Business Valuations versus Stock-Market Valuations

Graham writes:

The impact of market fluctuations upon the investor’s true situation may be considered also from the standpoint of the shareholder as the part owner of various businesses. The holder of marketable shares actually has a double status, and with it the privilege of taking advantage of either at his choice. On the one hand his position is analogous to that of a minority shareholder or silent partner in a private business. Here his results are entirely dependent on the profits of the enterprise or on a change in the underlying value of its assets. He would usually determine the value of such a private-business interest by calculating his share of the net worth as shown in the most recent balance sheet. On the other hand, the common-stock investor holds a piece of paper, an engraved stock certificate, which can be sold in a matter of minutes at a price which varies from moment to moment–when the market is open, that is–and often is far removed from the balance-sheet value.

Graham goes on to note that many successful businesses sell above their net worth. (Note that net worth is also called book value, balance-sheet value, asset value, net asset value, and tangible book value.) In this sense, Graham considers such businesses speculative as compared to unspectacular businesses selling at book value or below. (It should be noted that businesses with a sustainably high ROIC–return on invested capital–should sell above book value. Some successful technology companies fall into this category.)

Graham:

The previous discussion leads us to a conclusion of practical importance to the conservative investor in common stocks. If he is to pay some special attention to the selection of his portfolio, it might be best for him to concentrate on issues selling at a reasonably close approximation to their tangible-asset value–say, at not more than one-third above that figure. Purchases made at such levels, or lower, may with logic be regarded as related to the company’s balance sheet, and as having a justification or support independent of the fluctuating market prices….

(Illustration byTeguh Jati Prasetyo)

Graham adds:

A caution is needed here. A stock does not become a sound investment merely because it can be bought at close to its asset value. The investor should demand, in addition, a satisfactory ratio of earnings to price, a sufficiently strong financial position, and the prospect that its earnings will at least be maintained over the years. This may appear like demanding a lot from a modestly priced stock, but the prescription is not hard to fill under all but dangerously high market conditions. Once the investor is willing to forgo brilliant prospects–i.e., better than average expected growth–he will have no difficulty in finding a wide selection of issues meeting these criteria.

Graham then makes a central point:

The investor with a stock portfolio having such book values behind it can take a much more independent and detached view of stock-market fluctuations than those who have paid high multiples of both earnings and tangible assets. As long as the earning power of his holdings remains satisfactory, he can give as little attention as he pleases to the vagaries of the stock market. More than that, at times he can use these vagaries to play the master game of buying low and selling high.

The A. & P. Example

Graham gives the example of the Great Atlantic & Pacific Tea Co. The shares sold as high as $494 in 1929, and ended up declining to a new low of $36 in 1938. At that price, the company had a market capitalization of of $126 million, which was lower than its net current assets of $134 million. Essentially, the company was selling below net cash, which is cash minus all liabilities. So its value as a going concern was lower than its value in a liquidation would be. Graham explains:

Why? First, because there were threats of special taxes on chain stores; second, because net profits had fallen off in the previous year; and, third, because the general market was depressed. The first of these reasons was an exaggerated and eventually groundless fear; the other two were typical of temporary influences.

What about the investor who bought at $80 in 1937? Graham says the investor should carefully have studied the situation, but should have concluded that the market price was a temporary vagary. In fact, the investor should have bought more if he had the funds and the courage to do so.

By 1939, A. & P. was selling at $117.5. In the years following 1949, A. & P. continued to advance, eventually reaching a split-adjusted price of $705. At that price, the stock had a price-to-earnings ratio of 30, which implied that holders of the stock expected brilliant growth. Such expectations were not justified. The stock fell to an equivalent of $340, but even then was still not a bargain. Eventually if fell to the equivalent of $215 in 1970 and then $180 in 1972, when the company reported its first quarterly loss in its history.

Graham comments:

We see in this history how wide can be the vicissitudes of a major American enterprise in little more than a single generation, and also with what miscalculations and excesses of optimism and pessimism the public has valued its shares.

Graham concludes:

There are two chief morals to this story. The first is that the stock market often goes far wrong, and sometimes an alert and courageous investor can take advantage of its patent errors. The other is that most businesses change in character and quality over the years, sometimes for the better, perhaps more often for the worst. The investor need not watch his companies’ performance like a hawk; but he should give it a good, hard look from time to time.

Graham returns to the idea that a holder of marketable shares is like someone who owns a private business:

The true investor scarcely everis forced to sell his shares, and at all other times he is free to disregard the current price quotation. He need pay attention to it and act upon it only to the extent that it suits his book, and no more. Thus the investor who permits himself to be stampeded or unduly worried by unjustified market declines in his holdings is perversely transforming his basic advantage into a basic disadvantage. That man would be better off if his stocks had no market quotation at all, for he would then be spared the mental anguish caused him byother persons’ mistakes of judgment.

Graham then introduces the concept of “Mr. Market.” Imagine you own a share in a private business:

One of your partners, named Mr. Market, is very obliging indeed. Every day he tells you what he thinks your interest is worth and furthermore offers either to buy you out or to sell you an additional interest on that basis. Sometimes his idea of value appears plausible and justified by business developments and prospects as you know them. Often, on the other hand, Mr. Market lets his enthusiasm or his fears run away with him, and the value he proposes seems to you a little short of silly.

Graham makes the point that you do not form your opinion about the value of the business based on Mr. Market’s daily communication:

Only in case you agree with him, or in case you want to trade with him. You may be happy to sell out to him when he quotes you a ridiculously high price, and equally happy to buy from him when his price is low. But the rest of the time you will be wiser to form your own ideas of the value of your holdings, based on full reports from the company about its operations and financial position.

Graham argues that owning a share of stock is similar to the Mr. Market analogy:

Basically, price fluctuations have only one significant meaning for the true investor. They provide him with an opportunity to buy wisely when prices fall sharply and to sell wisely when they advance a great deal. At other times he will do better if he forgets about the stock market and pays attention to his dividend returns and to the operating results of his companies.

(Illustration by Andrii Vinnikov)

Graham concludes:

The investor with a portfolio of sound stocks should expect the prices to fluctuate and should neither be concerned by sizable declines nor become excited by sizable advances. He should always remember that market quotations are there for his convenience, either to be taken advantage of or to be ignored. He should never buy a stockbecauseit has gone up or sell onebecauseit has gone down.

Graham makes one final point:

Good managements produce a good average market price, and bad managements produce bad market prices.

CHAPTER 20: “MARGIN OF SAFETY” AS THE CENTRAL CONCEPT OF INVESTMENT

Graham writes:

In the old legend the wise men finally boiled down the history of mortal affairs into the single phrase, “This too will pass.” Confronted with a like challenge to distill the secret of sound investment into three words, we venture the motto, MARGIN OF SAFETY.

Graham comments:

Here the function of the margin of safety is, in essence, that of rendering unnecessary an accurate estimate of the future. If the margin is a large one, then it is enough to assume that future earnings will not fall far below those of the past in order for an investor to feel sufficiently protected against the vicissitudes of time.

Graham again:

The margin of safety is always dependent on the price paid. It will be large at one price, small at some higher price, nonexistent at some still higher price.

(Photo by Chuahtc8)

Graham explains margin of safety:

The margin-of-safety idea becomes much more evident when we apply it to the field of undervalued or bargain securities. We have here, by definition, a favorable difference between price on the one hand and indicated or appraised value on the other. That difference is the margin of safety. It is available for absorbing the effect of miscalculations or worse than average luck. The buyer of bargain issues places particular emphasis on the ability of the investment to withstand adverse developments. For in most such cases he has no real enthusiasm about the company’s prospects.

Graham goes on to note that a moderate decline in earnings power will not necessarily prevent a cheaply bought stock from producing a satisfactory investment result.

A Criterion of Investment versus Speculation

Graham writes:

Probably most speculators believe they have the odds in their favor when they take their chances, and therefore they may lay claim to a safety margin in their proceedings… But such claims are unconvincing. They rest on subjective judgment, unsupported by any body of favorable evidence or any conclusive line of reasoning. We greatly doubt whether the man who stakes money on his view that the market is heading up or down can ever be said to be protected by a margin of safety in any useful sense of the phrase.

Graham observes that, by contrast, buying stocks below a conservative appraisal of intrinsic value does imply a margin of safety and therefore does classify as investment rather than speculation.

To Sum Up

Graham sums up the chapter:

Investment is most intelligent when it is most businesslike. It is amazing to see how many capable businessmen try to operate in Wall Street with complete disregard of all the sound principles through which they have gained success in their own undertakings. Yet every corporate security may best be viewed, in the first instance, as an ownership interest in, or a claim against, a specific business enterprise. And if a person sets out to make profits from security purchases and sales, he is embarking on a business venture of his own, which must be run in accordance with accepted business principles if it is to have a chance of success.

Graham says the investor should know as much about the intrinsic values of the businesses in which he invests as he would need to know about the value of merchandise that he proposed to manufacture and sell.

Graham adds that the investor should be able to supervise adequately the running of the business in which he invests, and the investor should have confidence in the integrity and ability of the managers running the business.

Moreover, the investor should have a reasonable chance of profit, while possible losses should be minimal by comparison.

Furthermore, notes Graham, have the courage of your knowledge and experience, regardless of how many others agree or disagree.

You are neither right nor wrong because the crowd disagrees with you. You are right because your data and reasoning are right… in the world of securities, courage becomes the supreme virtueafter adequate knowledge and a tested judgment are at hand.

BOOLE MICROCAP FUND

An equal weighted group of micro caps generally far outperforms an equal weighted (or cap-weighted) group of larger stocks over time. See the historical chart here: https://boolefund.com/best-performers-microcap-stocks/

This outperformance increases significantly by focusing on cheap micro caps. Performance can be further boosted by isolating cheap microcap companies that show improving fundamentals. We rank microcap stocks based on these and similar criteria.

There are roughly 10-20 positions in the portfolio. The size of each position is determined by its rank. Typically the largest position is 15-20% (at cost), while the average position is 8-10% (at cost). Positions are held for 3 to 5 years unless a stock approachesintrinsic value sooner or an error has been discovered.

The mission of the Boole Fund is to outperform the S&P 500 Index by at least 5% per year (net of fees) over 5-year periods. We also aim to outpace the Russell Microcap Index by at least 2% per year (net). The Boole Fund has low fees.

If you are interested in finding out more, please e-mail me or leave a comment.

My e-mail: jb@boolefund.com

Disclosures: Past performance is not a guarantee or a reliable indicator of future results. All investments contain risk and may lose value. This material is distributed for informational purposes only. Forecasts, estimates, and certain information contained herein should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed.No part of this article may be reproduced in any form, or referred to in any other publication, without express written permission of Boole Capital, LLC.

Nassim Nicholas Taleb is the author of several books, including Fooled by Randomness, The Black Swan, and Antifragile. I wrote about Fooled by Randomness here: https://boolefund.com/fooled-by-randomness/

Today’s blog post is a summary of Taleb’s The Black Swan. If you’re an investor, or if you have any interest in predictions or in history, then this is a MUST-READ book. One of Taleb’s main points is that Black Swans, which are unpredictable, can be either positive or negative. It’s crucial to try to be prepared for negative Black Swans and to try to benefit from positive Black Swans. However, many measurements of risk in finance assume a statistical distribution that is normal when they should assume a distribution that is fat-tailed. These standard measures of risk won’t prepare you for a Black Swan.

That said, Taleb is an option trader, whereas I am a value investor. For me, if you buy a stock far below liquidation value, then usually you have a margin of safety. A group of such stocks will outperform the market over time while carrying low risk. Furthermore, if you’re a long-term investor, then you can either adopt a value investing approach or you can simply invest in low-cost index funds. Either way, given a long enough period of time, you should get good results. The market has recovered from every crash and has eventually gone on to new highs. Yet Taleb misses this point.

Nonetheless, although Taleb overlooks value investing and index funds, his views on predictions and on history are very insightful and should be studied by every thinking person.

Black Swan in Auckland, New Zealand. Photo by Angela Gibson.

Here’s the outline:

Prologue

PART ONE: UMBERTO ECO’S ANTILIBRARY, OR HOW WE SEEK VALIDATION

Chapter 1: The Apprenticeship of an Empirical Skeptic

Chapter 2: Yevgenia’s Black Swan

Chapter 3: The Speculator and the Prostitute

Chapter 4: One Thousand and One Days, or How Not to Be a Sucker

Chapter 5: Confirmation Schmonfirmation!

Chapter 6: The Narrative Fallacy

Chapter 7: Living in the Antechamber of Hope

Chapter 8: Giacomo Casanova’s Unfailing Luck: The Problem of Silent Evidence

Chapter 9: The Ludic Fallacy, or the Uncertainty of the Nerd

PART TWO: WE JUST CAN’T PREDICT

Chapter 10: The Scandal of Prediction

Chapter 11: How to Look for Bird Poop

Chapter 12: Epistemocracy, a Dream

Chapter 13: Apelles the Painter, or What Do You Do if You Cannot Predict?

PART THREE: THOSE GRAY SWANS OF EXTREMISTAN

Chapter 14: From Mediocristan to Extremistan, and Back

Chapter 15: The Bell Curve, That Great Intellectual Fraud

Chapter 16: The Aesthetics of Randomness

Chapter 17: Locke’s Madmen, or Bell Curves in the Wrong Places

Chapter 18: The Uncertainty of the Phony

PART FOUR: THE END

Chapter 19: Half and Half, or How to Get Even with the Black Swan

PROLOGUE

Taleb writes:

Before the discovery of Australia, people in the Old World were convinced that all swans were white, an unassailable belief as it seemed completely confirmed by empirical evidence… It illustrates a severe limitation to our learning from observations or experience and the fragility of our knowledge. One single observation can invalidate a general statement derived from millenia of confirmatory sightings of millions of white swans.

Taleb defines a black swan as having three attributes:

First, it is an outlier, as it lies outside the realm of regular expectations, because nothing in the past can convincingly point to its possibility.

Second, it carries an extreme impact.

Third, in spite of its outlier status, human nature makes us concoct explanations for its occurrence after the fact, making it explainable and predictable.

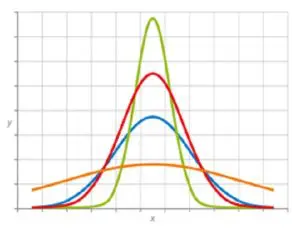

Taleb notes that the effect of Black Swans has been increasing in recent centuries. Furthermore, social scientists still assume that risks can be modeled using the normal distribution, i.e., the bell curve. Social scientists have not incorporated “Fat Tails” into their assumptions about risk. (A fat-tailed statistical distribution, as compared to a normal distribution, carries higher probabilities for extreme outliers.)

(Illustration by Peter Hermes Furian: The red curve is a normal distribution, whereas the orange curve has fat tails.)

Taleb continues:

Black Swan logic makes what you don’t know far more relevant than what you do know. Consider that many Black Swans can be caused and exacerbated by their being unexpected.

Taleb mentions the Sept. 11, 2001 terrorist attack on the twin towers. If such an attack had been expected, then it would have been prevented. Taleb:

Isn’t it strange to see an event happening precisely because it was not supposed to happen? What kind of defense do we have against that? … It may be odd that, in such a strategic game, what you know can be truly inconsequential.

Taleb argues that Black Swan logic applies to many areas in business and also to scientific theories. Taleb makes a general point about history:

The inability to predict outliers implies the inability to predict the course of history, given the share of these events in the dynamics of events.

Indeed, people, especially experts, have a terrible record in forecasting political and economic events. Taleb advises:

Black Swans being unpredictable, we need to adjust to their existence (rather than naively try to predict them). There are so many things we can do if we focus on antiknowledge, or what we do not know. Among many other benefits, you can set yourself up to collect serendipitous Black Swans (of the positive kind) by maximizing your exposure to them. Indeed, in some domains””such as scientific discovery and venture capital investments””there is a disproportionate payoff from the unknown, since you typically have little to lose and plenty to gain from a rare event… The strategy is, then, to tinker as much as possible and try to collect as many Black Swan opportunities as you can.

Taleb introduces the terms Platonicity and the Platonic fold:

Platonicity is what makes us think that we understand more than we actually do. But this does not happen everywhere. I am not saying that Platonic forms don’t exist. Models and constructions, these intellectual maps of reality, are not always wrong; they are wrong only in some specific applications. The difficulty is that a) you do not know before hand (only after the fact) where the map will be wrong, and b) the mistakes can lead to severe consequences…

The Platonic fold is the explosive boundary where the Platonic mindset enters in contact with messy reality, where the gap between what you know and what you think you know becomes dangerously wide. It is here that the Black Swan is produced.

PART ONE: UMBERTO ECO’S ANTILIBRARY, OR HOW WE SEEK VALIDATION

Umberto Eco’s personal library contains thirty thousand books. But what’s important are the books he has not yet read. Taleb:

Read books are far less valuable than unread books. The library should contain as much of what you do not know as your financial means, mortgage rates, and the currently tight real-estate market allow you to put there… Indeed, the more you know, the larger the rows of unread books. Let us call this collection of unread books an antilibrary.

Taleb adds:

Let us call an antischolar””someone who focuses on the unread books, and makes an attempt not to treat his knowledge as a treasure, or even a possession, or even a self-esteem enhancement device””a skeptical empiricist.

(Photo by Pp1)

CHAPTER 1: THE APPRENTICESHIP OF AN EMPIRICAL SKEPTIC

Taleb says his family is from “the Greco-Syrian community, the last Byzantine outpost in northern Syria, which included what is now called Lebanon.” Taleb writes:

People felt connected to everything they felt was worth connecting to; the place was exceedingly open to the world, with a vastly sophisticated lifestyle, a prosperous economy, and temperate weather just like California, with snow-covered mountains jutting above the Mediterranean. It attracted a collection of spies (both Soviet and Western), prostitutes (blondes), writers, poets, drug dealers, adventurers, compulsive gamblers, tennis players, apres-skiers, and merchants””all professions that complement one another.

Taleb writes about when he was a teenager. He was a “rebellious idealist” with an “ascetic taste.” Taleb:

As a teenager, I could not wait to go settle in a metropolis with fewer James Bond types around. Yet I recall something that felt special in the intellectual air. I attended the French lycee that had one of the highest success rates for the French baccalaureat (the high school degree), even in the subject of the French language. French was spoken there with some purity: as in prerevolutionary Russia, the Levantine Christian and Jewish patrician class (from Istanbul to Alexandria) spoke and wrote formal French as a language of distinction. The most privileged were sent to school in France, as both my grandfathers were… Two thousand years earlier, by the same instinct of linguistic distinction, the snobbish Levantine patricians wrote in Greek, not the vernacular Aramaic… And, after Hellenism declined, they took up Arabic. So in addition to being called a “paradise,” the place was also said to be a miraculous crossroads of what are superficially tagged “Eastern” and “Western” cultures.

Then a Black Swan hit:

The Lebanese “paradise” suddenly evaporated, after a few bullets and mortar shells… after close to thirteen centuries of remarkable ethnic coexistence, a Black Swan, coming out of nowhere, transformed the place from heaven to hell. A fierce civil war began between Christians and Moslems, including the Palastinian refugees who took the Moslem side. It was brutal, since the combat zones were in the center of town and most of the fighting took place in residential areas (my high school was only a few hundred feet from the war zone). The conflict lasted more than a decade and a half.

Taleb makes a general point about history:

The human mind suffers from three ailments as it comes into contact with history, what I call the triplet of opacity. They are:

the illusion of understanding, or how everyone thinks he knows what is going on in a world that is more complicated (or random) than they realize;

the retrospective distortion, or how we can assess matters only after the fact, as if they were in a rearview mirror (history seems clearer and more organized in history books than in empirical reality); and

the overvaluation of factual information and the handicap of authoritative and learned people, particularly when they create categories””when they “Platonify.”

Taleb points out that a diary is a good way to record events as they are happening. This can help later to put events in their context.

Taleb writes about the danger of oversimplification:

Any reduction of the world around us can have explosive consequences since it rules out some sources of uncertainty; it drives us to a misunderstanding of the fabric of the world. For instance, you may think that radical Islam (and its values) are your allies against the threat of Communism, and so you may help them develop, until they send two planes into downtown Manhattan.

CHAPTER 2: YEVGENIA’S BLACK SWAN

Taleb:

Five years ago, Yevgenia Nikolayevna Krasnova was an obscure and unpublished novelist, with an unusual background. She was a neuroscientist with an interest in philosophy (her first three husbands had been philosophers), and she got it into her stubborn Franco-Russian head to express her research and ideas in literary form.

Most publishers largely ignored Yevgenia. Publishers who did look at Yevnegia’s book were confused because she couldn’t seem to answer the most basic questions. “Is this fiction or nonfiction?” “Who is this book written for?” (Five years ago, Yevgenia attended a famous writing workshop. The instructor told her that her case was hopeless.)

Eventually the owner of a small unknown publishing house agreed to publish Yevgenia’s book. Taleb:

It took five years for Yevnegia to graduate from the “egomaniac without anything to justify it, stubborn and difficult to deal with” category to “persevering, resolute, painstaking, and fiercely independent.” For her book slowly caught fire, becoming one of the great and strange successes in literary history, selling millions of copies and drawing so-called critical acclaim…

Yevgenia’s book is a Black Swan.

CHAPTER 3: THE SPECULATOR AND THE PROSTITUTE

Taleb introduces Mediocristan and Extremistan:

Mediocristan

Extremistan

Nonscalable

Scalable

Mild or type 1 randomness

Wild (even superwild) type 2 randomness

The most typical member is mediocre

The most “typical” is either giant or dwarf, i.e., there is no typical member

Winners get a small segment of the total pie

Winner-take-almost-all effects

Example: Audience of an opera singer before the gramophone

Today’s audience for an artist

More likely to be found in our ancestral environment

More likely to be found in our modern environment

Impervious to the Black Swan

Vulnerable to the Black Swan

Subject to gravity

There are no physical constraints on what a number can be

Corresponds (generally) to physical quantities, i.e., height

Corresponds to numbers, say, wealth

As close to utopian equality as reality can spontaneously deliver

Dominated by extreme winner-take-all inequality

Total is not determined by a single instance or observation

Total will be determined by a small number of extreme events

When you observe for a while you can get to know what’s going on

It takes a long time to get to know what’s going on

Tyranny of the collective

Tyranny of the accidental

Easy to predict from what you see and extend to what you do not see

Hard to predict from past information

History crawls

History makes jumps

Events are distributed according to the “bell curve” or its variations

The distribution is either Mandelbrotian “gray” Swans (tractable scientifically) or totally intractable Black Swans

Taleb observes that Yevgenia’s rise from “the second basement to superstar” is only possible in Extremistan.

(Photo by Flavijus)

Taleb comments on knowledge and Extremistan:

What you can know from data in Mediocristan augments very rapidly with the supply of information. But knowledge in Extremistan grows slowly and erratically with the addition of data, some of it extreme, possibly at an unknown rate.

Taleb gives many examples:

Matters that seem to belong to Mediocristan (subjected to what we call type 1 randomness): height, weight, calorie consumption, income for a baker, a small restaurant owner, a prostitute, or an orthodontist; gambling profits (in the very special case, assuming the person goes to a casino and maintains a constant betting size), car accidents, mortality rates, “IQ” (as measured).

Matters that seem to belong to Extremistan (subjected to what we call type 2 randomness): wealth, income, book sales per author, book citations per author, name recognition as a “celebrity,” number of references on Google, populations of cities, uses of words in a vocabulary, numbers of speakers per language, damage caused by earthquakes, deaths in war, deaths from terrorist incidents, sizes of planets, sizes of companies, stock ownership, height between species (consider elephants and mice), financial markets (but your investment manager does not know it), commodity prices, inflation rates, economic data. The Extremistan list is much longer than the prior one.

Taleb concludes the chapter by introducing “gray” swans, which are rare and consequential, but somewhat predictable:

They are near-Black Swans. They are somewhat tractable scientifically””knowing about their incidence should lower your surprise; these events are rare but expected. I call this special case of “gray” swans Mandelbrotian randomness. This category encompasses the randomness that produces phenomena commonly known by terms such as scalable, scale-invariant, power laws, Pareto-Zipf laws, Yule’s law, Paretian-stable processes, Levy-stable, and fractal laws, and we will leave them aside for now since they will be covered in some depth in Part Three…

You can still experience severe Black Swans in Mediocristan, though not easily. How? You may forget that something is random, think that it is deterministic, then have a surprise. Or you can tunnel and miss on a source of uncertainty, whether mild or wild, owing to lack of imagination””most Black Swans result from this “tunneling” disease, which I will discuss in Chapter 9.

CHAPTER 4: ONE THOUSAND AND ONE DAYS, OR HOW NOT TO BE A SUCKER

Photo of turkey by Chris Galbraith

Taleb introduces the Problem of Induction by using an example from the philosopher Bertrand Russell:

How can we logically go from specific instances to reach general conclusions? How do we know what we know? How do we know that what we have observed from given objects and events suffices to enable us to figure out their other properties? There are traps built into any kind of knowledge gained from observation.

Consider a turkey that is fed every day. Every single feeding will firm up the bird’s belief that it is a general rule of life to be fed every day by friendly members of the human race “looking out for its best interests,” as a politician would say. On the afternoon of the Wednesday before Thanksgiving, something unexpected will happen to the turkey. It will incur a revision of belief.

The rest of this chapter will outline the Black Swan problem in its original form: How can we know the future, given knowledge of the past; or, more generally, how can we figure out properties of the (infinite) unknown based on the (finite) known?

Taleb says that, as in the example of the turkey, the past may be worse than irrelevant. The past may be “viciously misleading.” The turkey’s feeling of safety reached its high point just when the risk was greatest.

Roasted turkey. Photo by Alexander Raths.

Taleb gives the example of banking, which was seen and presented as “conservative,” based on the rarity of loans going bust. However, you have to look at the loans over a very long period of time in order to see if a given bank is truly conservative. Taleb:

In the summer of 1982, large American banks lost close to all their past earnings (cumulatively), about everything they ever made in the history of American banking””everything. They had been lending to South and Central American countries that all defaulted at the same time”””an event of an exceptional nature”… They are not conservative; just phenomenally skilled at self-deception by burying the possibility of a large, devastating loss under the rug. In fact, the travesty repeated itself a decade later, with the “risk-conscious” large banks once again under financial strain, many of them near-bankrupt, after the real-estate collapse of the early 1990s in which the now defunct savings and loan industry required a taxpayer-funded bailout of more than half a trillion dollars.

Taleb offers another example: the hedge fund Long-Term Capital Management (LTCM). The fund calculated risk using the methods of two Nobel Prize-winning economists. According to these calculations, risk of blowing up was infinitesimally small. But in 1998, LTCM went bankrupt almost instantly.

A Black Swan is always relative to your expectations. LTCM used science to create a Black Swan.

Taleb writes:

In general, positive Black Swans take time to show their effect while negative ones happen very quickly””it is much easier and much faster to destroy than to build.

Although the problem of induction is often called “Hume’s problem,” after the Scottish philosopher and skeptic David Hume, Taleb holds that the problem is older:

The violently antiacademic writer, and antidogma activist, Sextus Empiricus operated close to a millenium and a half before Hume, and formulated the turkey problem with great precision… We surmise that he lived in Alexandria in the second century of our era. He belonged to a school of medicine called “empirical,” since its practitioners doubted theories and causality and relied on past experience as guidance in their treatment, though not putting much trust in it. Furthermore, they did not trust that anatomy revealed function too obviously…

Sextus represented and jotted down the ideas of the school of the Pyrrhonian skeptics who were after some form of intellectual therapy resulting from the suspension of belief… The Pyrrhonian skeptics were docile citizens who followed customs and traditions whenever possible, but taught themselves to systematically doubt everything, and thus attain a level of serenity. But while conservative in their habits, they were rabid in their fight against dogma.

Taleb asserts that his main aim is how not to be a turkey.

In a way, all I care about is making a decision without being the turkey.

Taleb introduces the themes for the next five chapters:

We focus on preselected segments of the seen and generalize from it to the unseen: the error of confirmation.

We fool ourselves with stories that cater to our Platonic thirst for distinct patterns: the narrative fallacy.

We behave as if the Black Swan does not exist: human nature is not programmed for Black Swans.

What we see is not necessarily all that is there. History hides Black Swans from us and gives us a mistaken idea about the odds of these events: this is the distortion of silent evidence.

We “tunnel”: that is, we focus on a few well-defined sources of uncertainty, on too specific a list of Black Swans (at the expense of the others that do not easily come to mind).

CHAPTER 5: CONFIRMATION SHMONFIRMATION!

Taleb asks about two hypothetical situations. First, he had lunch with O.J. Simpson and O.J. did not kill anyone during the lunch. Isn’t that evidence that O.J. Simpson is not a killer? Second, Taleb imagines that he took a nap on the railroad track in New Rochelle, New York. He didn’t die during his nap, so isn’t that evidence that it’s perfectly safe to sleep on railroad tracks? Of course, both of these situations are analogous to the 1,001 days during which the turkey was regularly fed. Couldn’t the turkey conclude that there’s no evidence of any sort of Black Swan?

The problem is that people confuse no evidence of Black Swans with evidence of no possible Black Swans. Just because there has been no evidence yet of any possible Black Swans does not mean that there’s evidence of no possible Black Swans. Taleb calls this confusion the round-trip fallacy, since the two statements are not interchangeable.

Taleb writes that our minds routinely simplify matters, usually without our being consciously aware of it. Note: In his book, Thinking, Fast and Slow, the psychologist Daniel Kahneman argues that System 1, our intuitive system, routinely oversimplifies, usually without our being consciously aware of it.

Taleb continues:

Many people confuse the statement “almost all terrorists are Moslems” with “almost all Moslems are terrorists.” Assume that the first statement is true, that 99 percent of terrorists are Moslems. This would mean that only about .001 percent of Moslems are terrorists, since there are more than one billion Moslems and only, say, ten thousand terrorists, one in a hundred thousand. So the logical mistake makes you (unconsciously) overestimate the odds of a randomly drawn individual Moslem person… being a terrorist by close to fifty thousand times!

Taleb comments:

Knowledge, even when it is exact, does not often lead to appropriate actions because we tend to forget what we know, or forget how to process it properly if we do not pay attention, even when we are experts.

Taleb notes that the psychologists Daniel Kahneman and Amos Tversky did a number of experiments in which they asked professional statisticians statistical questions not phrased as statistical questions. Many of these experts consistently gave incorrect answers.

Taleb explains:

This domain specificity of our inferences and reactions works both ways: some problems we can understand in their applications but not in textbooks; others we are better at capturing in the textbook than in the practical application. People can manage to effortlessly solve a problem in a social situation but struggle when it is presented as an abstract logical problem. We tend to use different mental machinery””so-called modules””in different situations: our brain lacks a central all-purpose computer that starts with logical rules and applies them equally to all possible situations.

Note: Again, refer to Daniel Kahneman’s book, Thinking, Fast and Slow. System 1 is the fast-thinking intuitive system that works effortlessly and often subconsciously. System 1 is often right, but sometimes very wrong. System 2 is the logical-mathematical system that can be trained to do logical and mathematical problems. System 2 is generally slow and effortful, and we’re fully conscious of what System 2 is doing because we have to focus our attention for it to operate. See: https://boolefund.com/cognitive-biases/

Taleb next writes:

An acronym used in the medical literature is NED, which stands for No Evidence of Disease. There is no such thing as END, Evidence of No Disease. Yet my experience discussing this matter with plenty of doctors, even those who publish papers on their results, is that many slip into the round-trip fallacy during conversation.

Doctors in the midst of the scientific arrogance of the 1960s looked down at mothers’ milk as something primitive, as if it could be replicated by their laboratories””not realizing that mothers’ milk might include useful components that could have eluded their scientific understanding””a simple confusion of absence of evidence of the benefits of mothers’ milk with evidence of absence of the benefits (another case of Platonicity as “it did not make sense” to breast-feed when we could simply use bottles). Many people paid the price for this naive inference: those who were not breast-fed as infants turned out to be at an increased risk of a collection of health problems, including a higher likelihood of developing certain types of cancer””there had to be in mothers’ milk some necessary nutrients that still elude us. Furthermore, benefits to mothers who breast-feed were also neglected, such as a reduction in the risk of breast cancer.

Taleb makes the following point:

I am not saying here that doctors should not have beliefs, only that some kinds of definitive, closed beliefs need to be avoided… Medicine has gotten better””but many kinds of knowledge have not.

Taleb defines naive empiricism:

By a mental mechanism I call naive empiricism, we have a natural tendency to look for instances that confirm our story and our vision of the world””these instances are always easy to find…

Taleb makes an important point here:

Even in testing a hypothesis, we tend to look for instances where the hypothesis proved true.

Daniel Kahneman has made the same point. System 1 (intuition) automatically looks for confirmatory evidence, but even System 2 (the logical-mathematical-rational system) naturally looks for evidence that confirms a given hypothesis. We have to train System 2 not only to do logic and math, but also to look for disconfirming rather than confirming evidence. Taleb says:

We can get closer to the truth by negative instances, not by verification! It is misleading to build a general rule from observed facts. Contrary to conventional wisdom, our body of knowledge does not increase from a series of confirmatory observations, like the turkey’s.

Taleb adds:

Sometimes a lot of data can be meaningless; at other times one single piece of information can be very meaningful. It is true that a thousand days cannot prove you right, but one day can prove you to be wrong.

Taleb introduces the philosopher Karl Popper and his method of conjectures and refutations. First you develop a conjecture (hypothesis). Then you focus on trying to refute the hypothesis. Taleb:

If you think the task is easy, you will be disappointed””few humans have a natural ability to do this. I confess that I am not one of them; it does not come naturally to me.

Our natural tendency, whether using System 1 or System 2, is to look only for corroboration. This is called confirmation bias.

Illustration by intheskies

There are exceptions, notes Taleb. Chess grand masters tend to look at where their move might be weak, whereas rookie chess players only look for confirmation. Similarly, George Soros developed a unique ability to look always for evidence that his current hypothesis is wrong. As a result of this and not getting attached to his opinions, Soros quickly exited many of his trades that wouldn’t have worked. Soros is one of the most successful macro investors ever.

Taleb observes that seeing a red mini Cooper actually confirms the statement that all swans are white. Why? Because if all swans are white, then all nonwhite objects are not swans; in other words, the statement “if it’s a swan, then it’s white” is logically equivalent to the statement “if it’s not white, then it’s not a swan” (since all swans are white). Taleb:

This argument, known as Hempel’s raven paradox, was rediscovered by my friend the (thinking) mathematician Bruno Dupire during one of our intense meditating walks in London””one of those intense walk-discussions, intense to the point of our not noticing the rain. He pointed to a red Mini and shouted, “Look, Nassim, look! No Black Swan!”

Again: Finding instances that confirm the statement “if it’s not white, then it’s not a swan” is logically equivalent to finding instances that confirm the statement “if it’s a swan, then it’s white.” So consider all the objects that confirm the statement “if it’s not white, then it’s not a swan”: red Mini’s, gray clouds, green cucumbers, yellow lemons, brown soil, etc. The paradox is that we seem to gain ever more information about swans by looking at an infinite series of nonwhite objects.

Taleb concludes the chapter by noting that our brains evolved to deal with a much more primitive environment than what exists today, which is far more complex.

…the sources of Black Swans today have multiplied beyond measurability. In the primitive environment they were limited to newly encountered wild animals, new enemies, and abrupt weather changes. These events were repeatable enough for us to have built an innate fear of them. This instinct to make inferences rather quickly, and to “tunnel” (i.e., focus on a small number of sources of uncertainty, or causes of known Black Swans) remains rather ingrained in us. This instinct, in a word, is our predicament.

CHAPTER 6: THE NARRATIVE FALLACY

Taleb introduces the narrative fallacy:

We like stories, we like to summarize, and we like to simplify, i.e., to reduce the dimension of matters… The [narrative] fallacy is associated with our vulnerability to overinterpretation and our predilection for compact stories over raw truths. It severely distorts our mental representation of the world; it is particularly acute when it comes to the rare event.

Taleb continues:

The narrative fallacy addresses our limited ability to look at sequences of facts without weaving an explanation into them, or, equivalently, forcing a logical link, an arrow of relationship, upon them. Explanations bind facts together. They make them all the more easily remembered; they help them make more sense. Where this propensity can go wrong is when it increases our impression of understanding.

Taleb clarifies:

To help the reader locate himself: in studying the problem of induction in the previous chapter, we examined what could be inferred about the unseen, what lies outside our information set. Here, we look at the seen, what lies within the information set, and we examine the distortions in the act of processing it.

Taleb observes that our brains automatically theorize and invent explanatory stories to explain facts. It takes effort NOT to invent explanatory stories.

Taleb mentions post hoc rationalization. In an experiment, women were asked to choose from among twelve pairs of nylon stockings the ones they preferred. Then they were asked for the reasons for their choice. The women came up with all sorts of explanations. However, all the stockings were in fact identical.

Photo by Narokzaad

Split-brain patients have no connection between the left and right hemispheres of their brains. Taleb:

Now, say that you induced such a person to perform an act””raise his finger, laugh, or grab a shovel””in order to ascertain how how he ascribes a reason to his act (when in fact you know that there is no reason for it other than your inducing it). If you ask the right hemisphere, here isolated from the left side, to perform the action, then ask the other hemisphere for an explanation, the patient will invariably offer some interpretation: “I was pointing at the ceiling in order to…,” “I saw something interesting on the wall”…

Now, if you do the opposite, namely instruct the isolated left hemisphere of a right-handed person to perform an act and ask the right hemisphere for the reasons, you will be plainly told “I don’t know.”

Taleb notes that the left hemisphere deals with pattern recognition. (But, in general, Taleb warns against the common distinctions between the left brain and the right brain.)

Taleb gives another example. Read the following:

A BIRD IN THE

THE HAND IS WORTH

TWO IN THE BUSH

Notice anything unusual? Try reading it again. Taleb:

The Sydney-based brain scientist Alan Snyder… made the following discovery. If you inhibit the left hemisphere of a right-handed person (more technically, by directing low-frequency magnetic pulses into the left frontotemporal lobes), you will lower his rate of error in reading the above caption. Our propensity to impose meaning and concepts blocks our awareness of the details making up the concept. However, if you zap people’s left hemispheres, they become more realistic””they can draw better and with more verisimilitude. Their minds become better at seeing the objects themselves, cleared of theories, narratives, and prejudice.

Again, System 1 (intuition) automatically invents explanatory stories. System 1 automatically finds patterns, even when none exist.

Moreover, neurotransmitters, chemicals thought to transport signals between different parts of the brain, play a role in the narrative fallacy. Taleb:

It appears that pattern perception increases along with the concentration in the brain of the chemical dopamine. Dopamine also regulates moods and supplies an internal reward system in the brain (not surprisingly, it is found in slightly higher concentrations in the left side of the brains of right-handed persons than on the right side). A higher concentration of dopamine appears to lower skepticism and result in greater vulnerability to pattern detection; an injection of L-dopa, a substance used to treat patients with Parkinson’s disease, seems to increase such activity and lowers one’s suspension of belief. The person becomes vulnerable to all manner of fads…

Dopamine molecule. Illustration by Liliya623.

Our memory of the past is impacted by the narrative fallacy:

Narrativity can viciously affect the remembrance of past events as follows: we will tend to more easily remember those facts from our past that fit a narrative, while we tend to neglect others that do not appear to play a causal role in that narrative. Consider that we recall events in our memory all the while knowing the answer of what happened subsequently. It is literally impossible to ignore posterior information when solving a problem. This simple inability to remember not the true sequence of events but a reconstructed one will make history appear in hindsight to be far more explainable than it actually was””or is.

Taleb again:

So we pull memories along causative lines, revising them involuntarily and unconsciously. We continuously renarrate past events in the light of what appears to make what we think of as logical sense after these events occur.

One major problem in trying to explain and predict the facts is that the facts radically underdetermine the hypotheses that logically imply those facts. For any given set of facts, there exist many theories that can explain and predict those facts. Taleb:

In a famous argument, the logician W.V. Quine showed that there exist families of logically consistent interpretations and theories that can match a given set of facts. Such insight should warn us that mere absence of nonsense may not be sufficient to make something true.

There is a way to escape the narrative fallacy. Develop hypotheses and then run experiments that test those hypotheses. Whichever hypotheses best explain and predict the phenomena in question can be provisionally accepted.

The best hypotheses are only provisionally true and they are never uniquely true. The history of science shows that nearly all hypotheses, no matter how well-supported by experiments, end up being supplanted. Odds are high that the best hypotheses of today””including general relativity and quantum mechanics””will be supplanted at some point in the future. For example, perhaps string theory will be developed to the point where it can predict the phenomena in question with more accuracy and with more generality than both general relativity and quantum mechanics.

Taleb continues:

Let us see how narrativity affects our understanding of the Black Swan. Narrative, as well as its associated mechanism of salience of the sensational fact, can mess up our projection of the odds. Take the following experiment conducted by Kahneman and Tversky… : the subjects were forecasting professionals who were asked to imagine the following scenarios and estimate their odds.

Which is more likely?

A massive flood somewhere in America in which more than a thousand people die.

An earthquake in California, causing massive flooding, in which more than a thousand people die.

Most of the forecasting professionals thought that the second scenario is more likely than the first scenario. But logically, the second scenario is a subset of the first scenario and is therefore less likely. It’s the vividness of the second scenario that makes it appear more likely. Again, in trying to understand these scenarios, System 1 can much more easily imagine the second scenario and so automatically views it as more likely.

Next Taleb defines two kinds of Black Swan:

…there are two varieties of rare events: a) the narrated Black Swans, those that are present in the current discourse and that you are likely to hear about on television, and b) those nobody talks about, since they escape models””those that you would feel ashamed discussing in public because they do not seem plausible. I can safely say that it is entirely compatible with human nature that the incidences of Black Swans would be overestimated in the first case, but severely underestimated in the second one.

CHAPTER 7: LIVING IN THE ANTECHAMBER OF HOPE

Taleb explains:

Let us separate the world into two categories. Some people are like the turkey, exposed to a major blowup without being aware of it, while others play reverse turkey, prepared for big events that might surprise others. In some strategies and life situations, you gamble dollars to win a succession of pennies while appearing to be winning all the time. In others, you risk a succession of pennies to win dollars. In other words, you bet either that the Black Swan will happen or that it will never happen, two strategies that require completely different mind-sets.

Taleb adds:

So some matters that belong to Extremistan are extremely dangerous but do not appear to be so beforehand, since they hide and delay their risks””so suckers think they are “safe.” It is indeed a property of Extremistan to look less risky, in the short run, than it really is.

Illustration by Mariusz Prusaczyk

Taleb describes a strategy of betting on the Black Swan:

…some business bets in which one wins big but infrequently, yet loses small but frequently, are worth making if others are suckers for them and if you have the personal and intellectual stamina. But you need such stamina. You also need to deal with people in your entourage heaping all manner of insult on you, much of it blatant. People often accept that a financial strategy with a small chance of success is not necessarily a bad one as long as the success is large enough to justify it. For a spate of psychological reasons, however, people have difficulty carrying out such a strategy, simply because it requires a combination of belief, a capacity for delayed gratification, and the willingness to be spat upon by clients without blinking.

CHAPTER 8: GIACOMO CASANOVA’S UNFAILING LUCK: THE PROBLEM OF SILENT EVIDENCE

Taleb:

Another fallacy in the way we understand events is that of silent evidence. History hides both Black Swans and its Black Swan-generating ability from us.

Taleb tells the story of the drowned worshippers:

More than two thousand years ago, the Roman orator, belletrist, thinker, Stoic, manipulator-politician, and (usually) virtuous gentleman, Marcus Tullius Cicero, presented the following story. One Diagoras, a nonbeliever in the gods, was shown painted tablets bearing the portraits of some worshippers who prayed, then survived a subsequent shipwreck. The implication was that praying protects you from drowning. Diagoras asked, “Where were the pictures of those who prayed, then drowned?”

This is the problem of silent evidence. Taleb again:

As drowned worshippers do not write histories of their experiences (it is better to be alive for that), so it is with the losers in history, whether people or ideas.

Taleb continues:

The New Yorker alone rejects close to a hundred manuscripts a day, so imagine the number of geniuses that we will never hear about. In a country like France, where more people write books while, sadly, fewer people read them, respectable literary publishers accept one in ten thousand manuscripts they receive from first-time authors. Consider the number of actors who have never passed an audition but would have done very well had they had that lucky break in life.

Luck often plays a role in whether someone becomes a millionaire or not. Taleb notes that many failures share the traits of the successes:

Now consider the cemetery. The graveyard of failed persons will be full of people who shared the following traits: courage, risk taking, optimism, et cetera. Just like the population of millionaires. There may be some differences in skills, but what truly separates the two is for the most part a single factor: luck. Plain luck.

Of course, there’s more luck in some professions than others. In investment management, there’s a great deal of luck. One way to see this is to run computer simulations. You can see that by luck alone, if you start out with 10,000 investors, you’ll end up with a handful of investors who beat the market for 10 straight years.

(Photo by Volodymyr Pyndyk)

Taleb then gives another example of silent evidence. He recounts reading an article about the growing threat of the Russian Mafia in the United States. The article claimed that the toughness and brutality of these guys were because they were strengthened by their Gulag experiences. But were they really strengthened by their Gulag experiences?

Taleb asks the reader to imagine gathering a representative sample of the rats in New York. Imagine that Taleb subjects these rats to radiation. Many of the rats will die. When the experiment is over, the surviving rats will be among the strongest of the whole sample. Does that mean that the radiation strengthened the surviving rats? No. The rats survived because they were stronger. But every rat will have been weakened by the radiation.

Taleb offers another example:

Does crime pay? Newspapers report on the criminal who get caught. There is no section in The New York Times recording the stories of those who committed crimes but have not been caught. So it is with cases of tax evasion, government bribes, prostitution rings, poisoning of wealthy spouses (with substances that do not have a name and cannot be detected), and drug trafficking.

In addition, our representation of the standard criminal might be based on the properties of those less intelligent ones who were caught.

Taleb next writes about politicians promising “rebuilding” New Orleans after Hurricane Katrina:

Did they promise to do so with the own money? No. It was with public money. Consider that such funds will be taken away from somewhere else… That somewhere else will be less mediatized. It may be… cancer research… Few seem to pay attention to the victims of cancer lying lonely in a state of untelevised depression. Not only do these cancer patients not vote (they will be dead by the next ballot), but they do not manifest themselves to our emotional system. More of them die every day than were killed by Hurricane Katrina; they are the ones who need us the most””not just our financial help, but our attention and kindness. And they may be the ones from whom the money will be taken””indirectly, perhaps even directly. Money (public or private) taken away from research might be responsible for killing them””in a crime that may remain silent.

Giacomo Casanova was an adventurer who seemed to be lucky. However, there have been plenty of adventurers, so some are bound to be lucky. Taleb:

The reader can now see why I use Casanova’s unfailing luck as a generalized framework for the analysis of history, all histories. I generate artificial histories featuring, say, millions of Giacomo Casanovas, and observe the difference between the attributes of the successful Casanovas (because you generate them, you know their exact properties) and those an observer of the result would obtain. From that perspective, it is not a good idea to be a Casanova.

CHAPTER 9: THE LUDIC FALLACY, OR THE UNCERTAINTY OF THE NERD

Taleb introduces Fat Tony (from Brooklyn):

He started as a clerk in the back office of a New York bank in the early 1980s, in the letter-of-credit department. He pushed papers and did some grunt work. Later he grew into giving small business loans and figured out the game of how you can get financing from the monster banks, how their bureaucracies operate, and what they like to see on paper. All the while an employee, he started acquiring property in bankruptcy proceedings, buying it from financial institutions. His big insight is that bank employees who sell you a house that’s not theirs just don’t care as much as the owners; Tony knew very rapidly how to talk to them and maneuver. Later, he also learned to buy and sell gas stations with money borrowed from small neighborhood bankers.

…Tony’s motto is “Finding who the sucker is.” Obviously, they are often the banks: “The clerks don’t care about nothing.” Finding these suckers is second nature to him.

Next Taleb introduces non-Brooklyn John:

Dr. John is a painstaking, reasoned, and gentle fellow. He takes his work seriously, so seriously that, unlike Tony, you can see a line in the sand between his working time and his leisure activities. He has a PhD in electrical engineering from the University of Texas at Austin. Since he knows both computers and statistics, he was hired by an insurance company to do computer simulations; he enjoys the business. Much of what he does consists of running computer programs for “risk management.”

Taleb imagines asking Fat Tony and Dr. John the same question: Assume that a coin is fair. Taleb flips the coin ninety-nine times and gets heads each time. What are the odds that the next flip will be tails?

(Photo by Christian Delbert)

Because he assumes a fair coin and the flips are independent, Dr. John answers one half (fifty percent). Fat Tony answers, “I’d say no more than 1 percent, of course.” Taleb questions Fat Tony’s reasoning. Fat Tony explains that the coin must be loaded. In other words, it is much more likely that the coin is loaded than that Taleb got ninety-nine heads in a row flipping a fair coin.

Taleb explains:

Simply, people like Dr. John can cause Black Swans outside Mediocristan””their minds are closed. While the problem is very general, one of its nastiest illusions is what I call the ludic fallacy””the attributes of the uncertainty we face in real life have little connection to the sterilized ones we encounter in exams and games.

Taleb was invited by the United States Defense Department to a brainstorming session on risk. Taleb was somewhat surprised by the military people:

I came out of the meeting realizing that only military people deal with randomness with genuine, introspective intellectual honesty””unlike academics and corporate executives using other people’s money. This does not show in war movies, where they are usually portrayed as war-hungry autocrats. The people in front of me were not the people who initiate wars. Indeed, for many, the successful defense policy is the one that manages to eliminate potential dangers without war, such as the strategy of bankrupting the Russians through the escalation in defense spending. When I expressed my amazement to Laurence, another finance person who was sitting next to me, he told me that the military collected more genuine intellects and risk thinkers than most if not all other professions. Defense people wanted to understand the epistemology of risk.

Taleb notes that the military folks had their own name for a Black Swan: unknown unknown. Taleb came to the meeting prepared to discuss a new phrase he invented: the ludic fallacy, or the uncertainty of the nerd.

(Photo by Franky44)

In the casino you know the rules, you can calculate the odds, and the type of uncertainty we encounter there, we will see later, is mild, belonging to Mediocristan. My prepared statement was this: “The casino is the only human venture I know where the probabilities are known, Gaussian (i.e., bell-curve), and almost computable.”…

In real life you do not know the odds; you need to discover them, and the sources of uncertainty are not defined.

Taleb adds:

What can be mathematized is usually not Gaussian, but Mandelbrotian.

What’s fascinating about the casino where the meeting was held is that the four largest losses incurred (or narrowly avoided) had nothing to do with gambling.

First, they lost around $100 million when an irreplaceable performer in their main show was maimed by a tiger.

Second, a disgruntled contractor was hurt during the construction of a hotel annex. He was so offended by the settlement offered him that he made an attempt to dynamite the casino.

Third, a casino employee didn’t file required tax forms for years. The casino ended up paying a huge fine (which was the least bad alternative).

Fourth, there was a spate of other dangerous scenes, such as the kidnapping of the casino owner’s daughter, which caused him, in order to secure cash for the ransom, to violate gambling laws by dipping into the casino coffers.

Taleb draws a conclusion about the casino:

A back-of-the-envelope calculation shows that the dollar value of these Black Swans, the off-model hits and potential hits I’ve just outlined, swamp the on-model risks by a factor of close to 1,000 to 1. The casino spent hundreds of millions of dollars on gambling theory and high-tech surveillance while the bulk of their risks came from outside their models.

All this, and yet the rest of the world still learns about uncertainty and probability from gambling examples.

Taleb wraps up Part One of his book:

We love the tangible, the confirmation, the palpable, the real, the visible, the concrete, the known, the seen, the vivid, the visual, the social, the embedded, the emotionally laden, the salient, the stereotypical, the moving, the theatrical, the romanced, the cosmetic, the official, the scholarly-sounding verbiage (b******t), the pompous Gaussian economist, the mathematicized crap, the pomp, the Academie Francaise, Harvard Business School, the Nobel Prize, dark business suits with white shirts and Ferragamo ties, the moving discourse, and the lurid. Most of all we favor the narrated.

Alas, we are not manufactured, in our current edition of the human race, to understand abstract matters””we need context. Randomness and uncertainty are abstractions. We respect what had happened, ignoring what could have happened.

PART TWO: WE JUST CAN’T PREDICT

Taleb:

…the gains in our ability to model (and predict) the world may be dwarfed by the increases in its complexity””implying a greater and greater role for the unpredicted.

CHAPTER 10: THE SCANDAL OF PREDICTION

Taleb highlights the story of the Sydney Opera House:

The Sydney Opera House was supposed to open in early 1963 at a cost of AU$ 7 million. It finally opened its doors more than ten years later, and, although it was a less ambitious version than initially envisioned, it ended up costing around AU$ 104 million.

Taleb then asks:

Why on earth do we predict so much? Worse, even, and more interesting: Why don’t we talk about our record in predicting? Why don’t we see how we (almost) always miss the big events? I call this the scandal of prediction.

The problem is that when our knowledge grows, our confidence about how much we know generally increases even faster.

Illustration by Airdone.

Try the following quiz. For each question, give a range that you are 90 percent confident contains the correct answer.

What was Martin Luther King, Jr.’s age at death?